http://www.freepressjournal.in/analysis/rn-bhaskar-energy-prices-favour-india-may-be-not-opec/1085442

Oil prices favour India, for now

— By | Jun 15, 2017 07:15 am

The snapping of diplomatic ties with Qatar by many Arab countries underlines the precariousness of oil politics. Much of the Middle Eastern politics are on account of, and have a direct bearing on, oil and gas. In fact, many speculators expect oil prices to harden after the Qatar development. But that might not happen.

Three things went against Qatar. First, it rankled many Arab states by managing its own wealth very successfully. Envy can be a great driver for hatred. Second, were reports that it has been supporting Iran which is a Shia country compared to many Arab states which are Sunni. Third, Qatar exports a clean fuel – liquefied natural gas or LNG – which oil producers (including the USA) blame for many of their current problems.

It was, therefore, not entirely surprising that some Arab states would gang up against Qatar. But what was laughable was the theory that Qatar was promoting terrorism. More terror funding has been supported by Saudi Arabia and even Pakistan. Possibly, oil politics –and US disinformation — overshadowed sound reasoning.

It was, therefore, not entirely surprising that some Arab states would gang up against Qatar. But what was laughable was the theory that Qatar was promoting terrorism. More terror funding has been supported by Saudi Arabia and even Pakistan. Possibly, oil politics –and US disinformation — overshadowed sound reasoning.

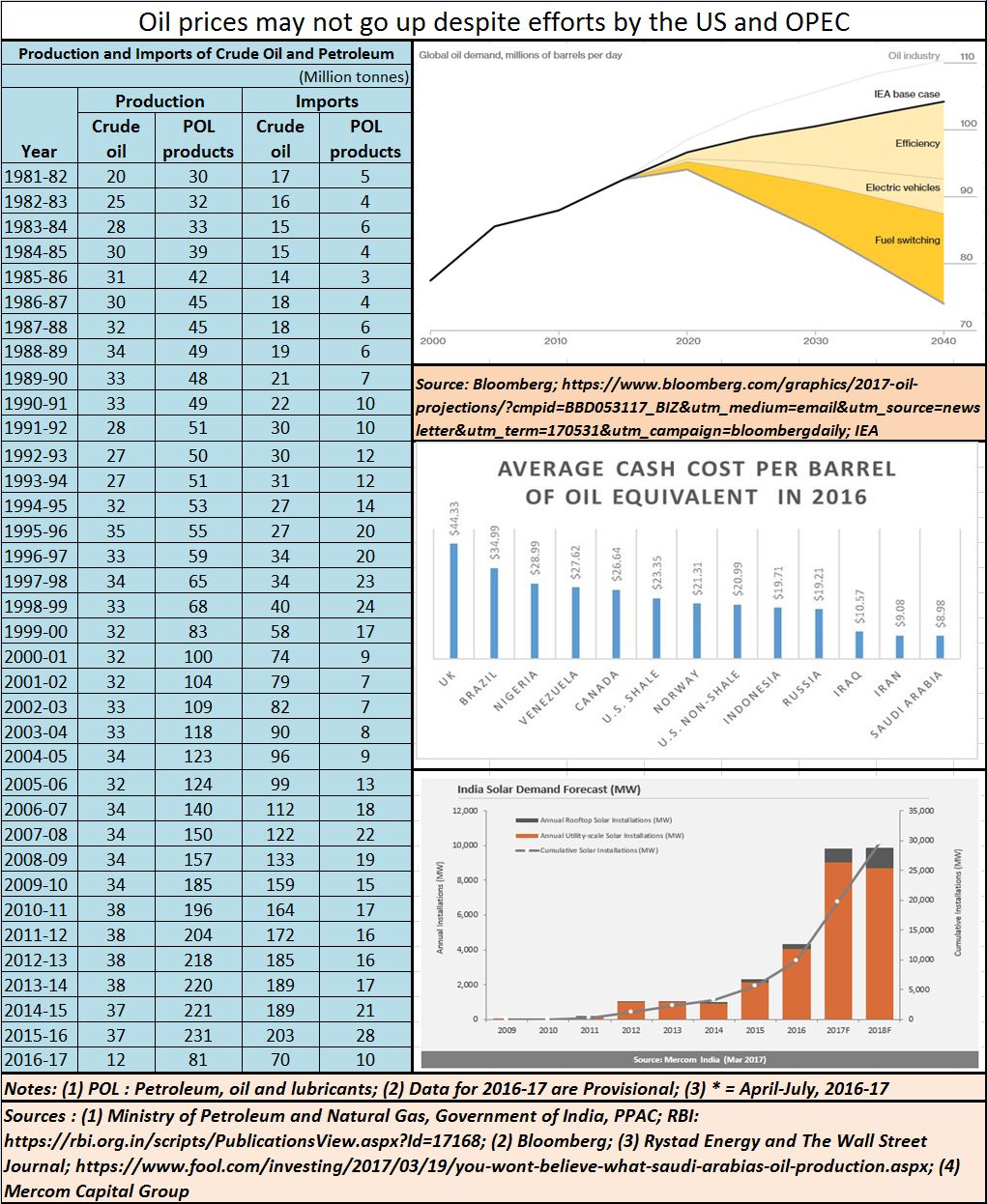

The oil lobby is very strong in the US and is known to support many political campaigns. It is also most opposed to any support for fuel efficiency or reduction of greenhouse emissions, as that would affect the demand for petrol and diesel. This lobby also dislikes shale gas producers who, it believes, caused oil prices to tumble worldwide.

Shale gas producers have also been nimble. Despite a sharp decline in the use of oil rigs, innovative approaches have helped oil and gas production to keep increasing. Oil prices slipped from over $100 to under $30 a barrel.

At $30, many shale gas producers began to shut down operations. Oil producers were jubilant. But what they did not reckon with is that shale gas producers take little time to shut down operations and to restart them. As soon as oil prices climbed, shale gas producers were back in business. Oil prices began climbing but not too much. Any price over $30 was just about affordable to shale gas producers (their cost is a bit over $23 – see chart).

Countries like Saudi Arabia, Iraq and Iran didn’t really lose money. Their cost per barrel of production is believed to be under $10 a barrel. But they aren’t making as much money as before. Qatar’s costs are not known, but they are believed to be under $10. And it remains the largest exporter of LNG to the world. During its hey days, it could command prices of over $17 per MMBTU (Million British Thermal Units), but now they’ve slipped to under $10. Saudi Arabia does not like this, because LNG is proving to be not only cheaper, but is also a cleaner fuel than oil.

Countries like Saudi Arabia, Iraq and Iran didn’t really lose money. Their cost per barrel of production is believed to be under $10 a barrel. But they aren’t making as much money as before. Qatar’s costs are not known, but they are believed to be under $10. And it remains the largest exporter of LNG to the world. During its hey days, it could command prices of over $17 per MMBTU (Million British Thermal Units), but now they’ve slipped to under $10. Saudi Arabia does not like this, because LNG is proving to be not only cheaper, but is also a cleaner fuel than oil.

Add to this another headache. The vision that Hermann Scheer (former minister of energy in Germany) had for solar power (http://www.asiaconverge.com/2016/04/india-not-learn-germanys-hermann-scheer-solar-power-model/) is actually becoming a reality. With less than 1% of the subsidies that the oil industry has enjoyed, solar power prices have tumbled year after year since the turn of this century. In India, they tumbled from over Rs.10.5 per kWh in 2011 to Rs.2.44/kWh – the lowest bid in the Bhadla Solar Park (250 MW). Some say that this price conceals hidden subsidies. But if one examines the lowest bid in the US without subsidies, solar power costs (20 year power purchase agreements) have reached under 3 cents a unit level (http://www.freepressjournal.in/indias-expensive-solar-power-birth-pangs/). Battery prices also continue to fall (http://www.asiaconverge.com/2015/06/battery-a-dirge-for-fossil-fuels/). Bloomberg expects them to continue declining over the next decade. Clearly, the scope for solar power costs falling further cannot be ruled out (http://www.asiaconverge.com/2016/07/solar-methane-better-days-ahead/).

All this will help reduce the demand for oil.

That is why, even though EIA predicts oil prices to go up to $100 a barrel (https://www.bloomberg.com/graphics/2017-oil-projections/?cmpid=BBD053117_BIZ&utm_medium=email&utm_source=newsletter&utm_term=170531&utm_campaign=bloombergdaily), Bloomberg expects it to languish at under $80 (see chart). If Russia or Iran ramps up its own production, prices could slip further.

That will help India escape a surging import bill. And if India plays the solar and methane generation game carefully, it could actually become net positive on the oil front. India is, after all, a producer of oil and gas as well (see table).

If India wants to win this game, it must focus on decentralized cluster power generation and methane generation on a nationwide scale (Maharashtra has already begun examining its feasibility). But to do this, it must stop getting distracted by needless and unnecessary issues like bans and exclusions. It is not wise to lose jobs especially when job creation is abysmally low.

The possibilities for India are both breathtaking and exciting. But the government will have to work on this positive potential. India needs to stop thinking in terms of bans and closures – irrespective of whether they relate to books, cinema, plays or cattle. There is work ahead. The potential is there. The future beckons. Can India rise to the occasion?

{kind=link}

COMMENTS