The Indian private sector is doing better than imagined by many

Read Part II of this article here.

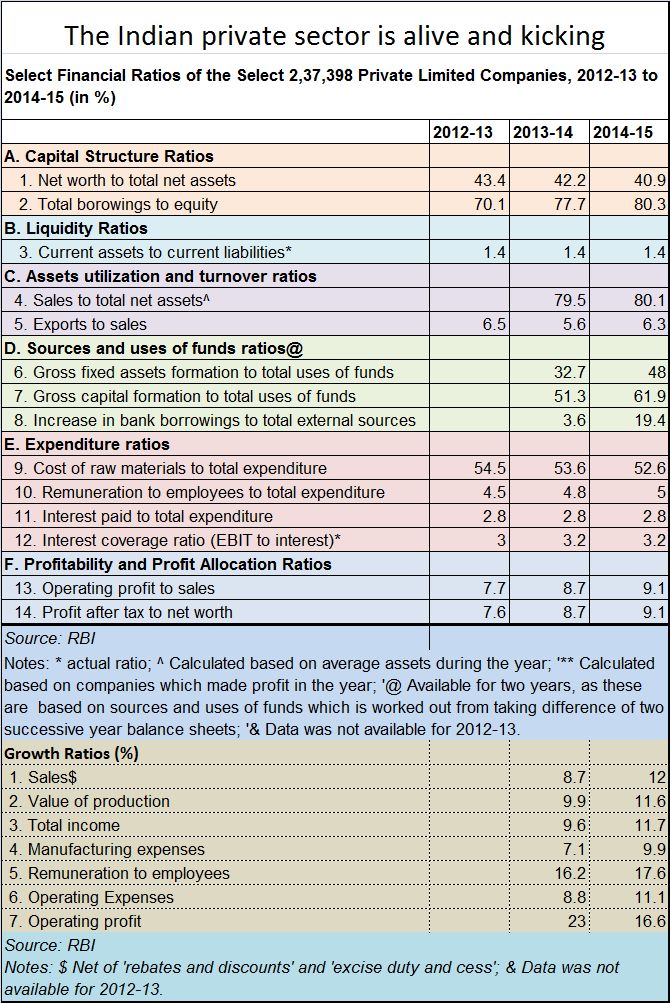

The Reserve Bank of India (RBI) has just released data on the finances of 237,398 non-government non-financial (NGNF) private limited companies. It shows how India’s private sector companies are still doing quite well.

Reuters

Contrary to statements one hears of so often, the RBI data shows that on an average the financial ratios of these companies have been quite good (see chart).

Analysing the RBI data, the Mint (a publication belonging to the HT group) talked about how small units are considered inefficient compared with their large-scale counterparts. They are shackled by regulations, inadequate availability of credit and finance — especially equity capital — orthodox marketing and lack of access to global markets and adequate skills. Archaic processes and a reluctance to use information and communications technology further hobble them.

But then watch the numbers. Watch how the cost of raw materials to total expenditure has climbed down. Payment to the workforce has gone up. Yet profitability is higher. This can happen only if the operations at manufacturing units come down through sheer efficiency. The Indian corporate sector has done India proud.

It is reasonable to assume that much of this growth and profitability took place not because of large companies, but because of the MSME (micro, small and medium enterprises) sector.

It is reasonable to assume that much of this growth and profitability took place not because of large companies, but because of the MSME (micro, small and medium enterprises) sector.

That is because almost 80% of these companies are likely to be those who get categories as MSMEs sector accounts for 48 million enterprises. This sector contributes to 37.5% to India’s gross domestic product. More crucially, it provides employment to 111.4 million persons and accounts for more than 40% of India’s exports. In other words, the MSME sector is more relevant to India than the medium and the large sectors.

But why should the MSME sector do so much better than large units? The answer is simple. They work harder, with few of the perquisites that the larger companies enjoy. This is despite the fact that many of the MSMEs have to borrow money from non-conventional sources, often at interest rates that are higher than 2% a month.

And they are more responsible borrowers. While larger units have enjoyed debt equity ratios of over 1.5:1, the average in the chart alongside shows that for all companies put together, the average debt was just around 80% of equity. This number looks lower primarily because the MSME works on extremely low debt.

As the next part will show, much of the default on loans from banks is also on account of medium and large companies, and not the small industries sector.

{kind=link}

COMMENTS