MARKET PERSPECTIVE

By J Mulraj

Aug 16-22, 2025

A P&L of the Ukraine war reveals the futility of it

Image created by Bing

The Collective West is responsible for starting and sustaining the Ukraine war by:

> Asking Germany to cancel contracts to receive Russian gas via the two Nordstream pipelines.

> Then blowing up both pipelines.

> Considering NATO membership for Ukraine, despite assurances NATO would not expand Eastwards, and ignoring Russian warnings that it was a red line they shouldn’t cross (missiles placed in a NATO country, Ukraine, gives Moscow insufficient time to intercept; a re-run of the Cuban missile crisis).

> Sending Boris Johnson, then PM of the United Kingdom, to tear up a ceasefire agreement both Ukraine and Russia had willingly entered into, a month after the invasion began, under which Ukraine would have retained all of it’s territory.

> Prolonging the war through financial and military aid, (which emptied their treasuries and their armouries).

It’s been over three years since this lunatic provocation of the Russian bear began. It’s aim was to weaken Russia through a proxy war against Ukraine, thereby outsourcing war deaths to Ukraine and destroying it’s infrastructure and resources.

Towards what aim? Has the aim been achieved?

- To weaken Russia: No. If it had, why would Sweden and Finland seek NATO membership? And why would Trump arm twist EU to raise defence spending from 2 to 5%?

- To give Ukraine, a democracy, the right to join NATO: It hasn’t been achieved. Puin’s conditions insist it will not join.

- To control Russia’s crude oil: The Collective West wanted the production, about 10% of global supply for itself, at a discount. If supply of 10% of global supply vanishes, price of oil will shoot up, causing a global recession. The West hates that China and India are getting discounted oil. It isn’t.

The leadership of Ukraine should do a P&L analysis of it’s gains from the war and its losses.

One can honestly see no gains. If ever there was a one-sided P&L, this is it.

- In losses, Ukraine has, reportedly, lost between 3 – 5 million people in the war. It’s population is now 37.9 m., as per Politico, down from 41-43 m before the war started. It used to be 52 m. when it gained independence from the Soviet Union in 1991.

- Suffered the loss of millions of young people who have emigrated out of Ukraine. As a result of deaths and emigration, the fertility rate (number of babies per woman) of Ukraine is 1.3, one of the lowest in the world. The rate needed to sustain a population is 2.1. In essence, Ukraine, as a society, is doomed to disappear, unless it allows immigration in big numbers. Even then, without integration, its way of life is gone. That’s the cost of the war inflicted on Ukraine, because of the Collective West provoking Russia, and later tearing up peace terms agreed upon by both sides, a month after the invasion, if Zelenskyy had agreed not to opt for NATO membership.

- Had it’s infrastructure destroyed, inhibiting its post-war recovery by exploiting its reserves of rare earth minerals. Ukraine holds about 5% of global rare earth minerals. However, these reserves are yet to be surveyed for commercial viability and, in any case, lie in areas Russia has captured and is unwilling to return.

Hence the P&L of Ukraine’s war is covered with red ink.

Will the summit meeting between Putin and Trump, recently held in Alaska, lead to a peace agreement?

It is highly unlikely as there is a chasm between the two sides of what such an agreement would look like.

Stumbling blocks

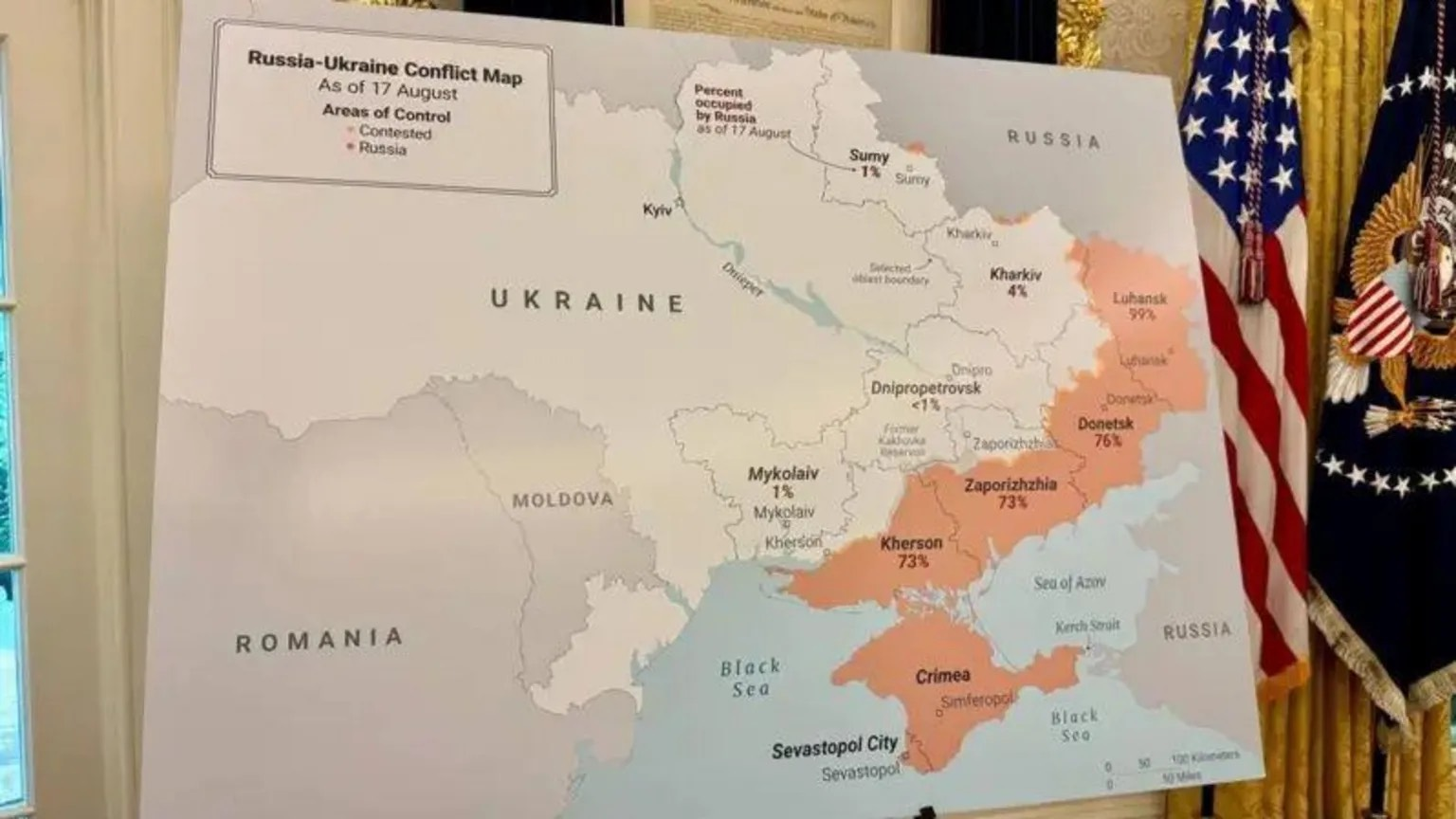

Territorial Claims are the first hurdle.

The map above, presented by Russia, shows, in orange, the Ukrainian territory it has captured, with a % of the region represented held by it. It wants the entire Donbas region ( Donetsk and Luhansk), asking for the balance region needed to reach 100%, to be ceded by Ukraine. Russia wants to retain Kherson and Zeporizhzhia it has captured, and is willing to swap other regions with Ukraine. The demand is based on the dictum ‘to the winner goes the spoils of war’.

Zelenskyy says that the Constitution of Ukraine does not allow ceding of territory. Having fought a war and lost it, he cannot hold up the Constitution to deter the reality.

Security Guarantees

Ukraine seeks security guarantees to protect it from future attacks by Russia. The starting point of the war was the Russian red line against NATO/US weapons, or soldiers, to be placed in Ukraine, where they pose an existential threat to Russia. A missile fired from Ukraine would hit Moscow in minutes, with not enough time to intercept it.

Having fought a war for over 3 years over this red line it’s difficult to see how Russia would accept a security guarantee, as sought by Ukraine, involving establishing missiles and US/EU boots on the ground.

Moreover, Ukraine is seeking, as a part of the security guarantee, a huge sum of money to re-arm itself and to rebuild its infrastructure. Putin has stated that Ukraine could build defensive capacity but not offensive capability to attack Russia with.

So the ‘security guarantee’ would become a stumbling block.

Funding the security guarantee and reconstruction

US VP, J D Vance, has stated that the bulk of the financial burden of both the security guarantee and the reconstruction, would have to be borne by Europe, as this was a European war.

EU countries have, under US pressure, agreed to raise NATO contributions to 5% of GDP.

Can they afford to? Debt to GDP levels are already high in Italy (135%), France (112%) and UK (95%). The Social Security systems in all are underfunded and so are their healthcare systems. So, when push comes to shove, will they water down Ukrainian demands?

Stock markets should not assume an early peace treaty. Of course, if diplomacy fails to deliver an end to the war, a military solution may deliver it. Ukraine has a hugely depleted and demoralised military.

Last week, the BSE Sensex closed at 81306 for a weekly gain of 709 points.

In 1964 the per capita incomes of both India and China were equal. India’s policy makers continued with socialist policies, distrusting the private sector, and stunting it’s growth with a myopic licensing policy and laws like MRTP (Monopolies & Restrictive Trade Practices) Act. The irony that their own licensing policies created the monopolies was lost on them. China, under Deng Xiaoping, opened up in ‘80s; India in 1992 after ‘empty coffers’.

Today China’s per capita GDP is 5X India’s.

The reason for reiterating this is that remnants of such suspicion towards the private sector still remain. And this translates to inordinately high GST rates of 5%, 12%, 18% and 24%. It’s surprising that the auto industry, with a high employment multiplier effect, bears GST at 28%, the highest rate. This indicates the myopic attitude, still persisting, of the car being a “luxury”, needing to attract the highest rate.

Fortunately, GST rates will henceforth be in 2 slabs, 5 and 18%, a step in the right direction, but more steps should be taken.

Kyndryl, accompany spun off from IBMs IT infrastructure service business, is to invest $ 2.25 b in India, over three years, to develop IT talent, AI innovation, and support digital training. It has opened a 250,000 sq feet office space in Bengaluru. This, again, reveals the pathetic views of politicians. When Mr Narayan Murthy, the visionary and reputable founder of Infosys, had petitioned for better roads to enable foreign customers to reach their destination for doing business faster, Shri Deve Gowda had, wrongly, called him a land grabber. Times have changed. Kyndryl was able to acquire a quarter million sq feet office without a pejorative and unfounded accusation.

A distressing piece of news is that, of the 193 cases filed in the last decade by the Enforcement Directorate, against elected Government officials, only 2 charges have been proven.

Does India have a judicial animal farm? Is the polity more equal than others? This HAS to stop.

That stock markets are steady amongst a backdrop of physical and trade wars, can only be explained away as a triumph of hope over analysis.

Prudence is the better part of valour.

Comments may be sent to jmulraj@asiaconverge.com

{kind=link}

COMMENTS