R N Bhaskar

9 March 2015

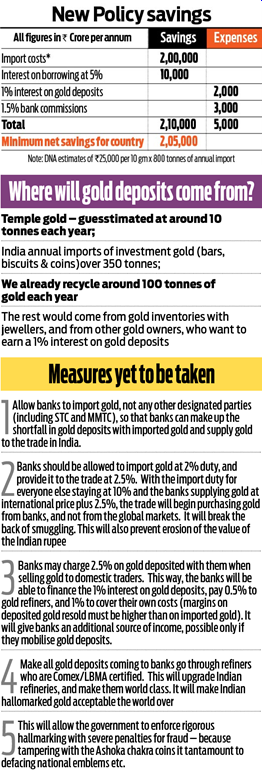

The gold policy announced by Arun Jaitley, Union finance minister, is both path-breaking and meaningful. First, take the maths. India imports around 800-1,000 tonnes of gold annually. Some of it gets re-exported (as jewellery). But if you take 800 tonnes, and multiply this with a figure of Rs25,000 per 10 grammes, you arrive at a whopping figure of Rs200,000 crore (see chart alongside).

Second, look at the industry structure. Much of this gold goes into making jewellery, some even gets exported. But some of it — around 300 tonnes each year — comes into India by way of gold bars, biscuits and coins.

These are often referred to as investment gold. Then there is recycled gold which contributes almost 100 tonnes (15%) to India’s annual gold demand. Globally, it enjoys a higher share of over 30% of the 176,000 tonnes of annual demand. This could be scrap that jewellers are left with while converting this metal into jewellery. It could be gold from pawnbrokers, or it could be temple gold. For instance, just last year, the Tirumala Trust (which runs the famous Tirupati group of temples) deposited 1.8 tonnes of gold with the State Bank of India. This gold is eventually melted down, refined and recycled.

Globally, gold is also recovered from discarded electronic items, contributing to 10% of annual consumption. Now any type of gold can be deposited with banks. If all goes well, the benefits could be staggering. This is because India’s horde of gold in private hands is the largest in the world. The government estimates this to be 20,000 tonnes, though many in the trade put this number at 25,000 tonnes.

Will people be willing to deposit gold with Indian banks? Yes, if the bold innovations announced by Turkey a few years ago are any indication. In just four years, Turkey has managed to persuade people to part with a total of around 500 tonnes (25%) of gold from an estimated 2,000 tonnes of gold in private hands, which Turkey calls under-the-pillow gold. India could easily mop up at least 10% of its own under-the-pillow gold.

That would allow the government to give to the Indian gold trade the 800-odd tonnes its needs each year from domestic sources for the next two years. It will means forex savings of Rs200,000 crore each year. If one assumes a 5% cost for purchasing this gold (interest plus insurance plus freight), India could be saving another Rs10,000 crore annually.

Even after adjusting for the 1% interest to be paid to gold depositors, 0.5% to approved refiners, and accounting for the bank’s own margins, the cost would be under Rs5,000 crore, less than Rs10,000 crore for importing the gold into India. However, such a scheme can work only if people have confidence in the gold the banks sell, and the honesty with which they assay the gold brought in as deposits.

That is why it is imperative that, as in Turkey, banks play a critical role. Import of gold and gold deposits should be through banks only — not even MMTC or STC.

Second, banks must align themselves with LBMA/Comex certified gold refineries. These certifying agencies invariably audit business practices, and examine the manner in which gold inventories are kept, regularly. They ensure that the gold refined is never sub-standard; the penalties for not abiding by these globally respected norms can be harsh and swift.

Third, the government should also open a window for people to declare their concealed gold — against payment of prescribed penalties — failing which the consequences could be painful, as they would include imprisonment (outlined in the budget speech last fortnight).

Guaranteed quality, and easy access, will make the Ashoka symbol on the gold coins a rage with customers. First, because they will be available at a discount to the Krugerrand (South Africa) or the Swiss gold bars and biscuits (because domestic sourcing and availability will mean lower transportation and insurance costs). Second, because they are backed by LMBA/Comex certification.

If standards are maintained, and rigorously enforced across the country through hallmarking, India will soon become a gold hub, far more vibrant than the gold souks of the Middle East. The gold jewellery trade already employs over 3.5 crore people. This number could double, as the trade is allowed to become vibrant and healthy.

Over a period of time, Indian consumers will also learn that converting gold into jewellery involves making charges. They will soon begin putting their surplus money — after meeting the requirements for tradition-bound events like marriage and childbirth — in gold coins and biscuits. That will gradually draw out more gold from Indian homes as deposits. And the ghost of smuggling could finally get exorcised.

Will that hurt Indian jewellers? Not really. Scrupulous hallmarking will catapult this industry into healthier exports and better premiums. After years of being merely an import market, India could become an export hub too.

Instead of fattening the foreigner, the government is finally promoting the Indian. The budget proposals could make gold smuggling unattractive. And they could usher in fresh vision; allowing the markets to create more gold-related products to suit various investment needs.

India could easily emerge as the ultimate global destination for gold as well as for gems and jewellery.

The author is consulting editor with DNA.

Read the original article here.

More on India and its policies here.

{kind=link}

COMMENTS