http://www.freepressjournal.in/analysis/rn-bhaskar-epayments-the-government-stumbles-again/1023892

Epayments – several things the RBI and the Cabinet Secretary overlooked

— By | Feb 23, 2017 08:59 am

Last week, the government came out with two announcements regarding epayments. One was through the Reserve Bank of India (RBI). The other was through the cabinet secretariat.

The RBI announcement creates rules of merchant discount rates (MDRs) and also allows for stakeholders to post their responses with it by 28 February. The Cabinet Secretariat announcement has no such provision. It is an order. Period. The order from the Cabinet Secretary known as “Promotion of digital transactions including digital payments” delegates this job to the Ministry of Electronics and Information Technology (Meity). Accordingly, on Thursday last, the President of India gave his consent to amend the “Government of India, Allocation of Business Rules, 1963” assigning this new responsibility to Meity.

The RBI announcement creates rules of merchant discount rates (MDRs) and also allows for stakeholders to post their responses with it by 28 February. The Cabinet Secretariat announcement has no such provision. It is an order. Period. The order from the Cabinet Secretary known as “Promotion of digital transactions including digital payments” delegates this job to the Ministry of Electronics and Information Technology (Meity). Accordingly, on Thursday last, the President of India gave his consent to amend the “Government of India, Allocation of Business Rules, 1963” assigning this new responsibility to Meity.

Both orders are short sighted, and both hold out implications that do not bode well for epayment as an industry and the finance sector in general.

Take the Cabinet Secretariat order to start with. All promotion of epayment is supposed to be linked to some basic rules of business. These rules are usually framed by the ministry of finance, the RBI and the banking sector. By transferring the promotion of epayment to Meity, the government has allowed the same job to be done by two masters. That is both unwise and illogical.

Meity’s job is to promote fair access rules, transparency and network access across the country. Its job is to ensure that there is no regulatory capture in the business – whether by telecom companies or internet players. The job of promoting a particular business activity should be left to the industry concerned. By bringing in Meity, the government has allowed for more government and less governance. Both ministries will end up blaming each other for any shortcomings. This must be avoided.

The RBI note – though it allows for consultation — is also flawed. And there are several reasons for making this charge:

- The government is as much a player in the epayment and digitisation business, as is the rest of the industry. There is no need for the government to be treated as a separate category with different rules than those applicable for other industry players.

- The present set of guidelines will promote more confusion and dispute. For instance, will a state government owned electric supply company (discom) be treated as a government entity or a service provider? Ditto with organizations like MTNL.

- The RBI circular is silent about the role played by private entities like PayU.in often partnership with municipal corporations and other state bodies. Some of these portals deny access to epayment players like Mastercard, Visa and even Rupay (http://www.asiaconverge.com/2017/01/epayments-an-scam-potential/).

- The RBI is silent on whether the flat fee payment mechanism will seek to exclude players like Rupay, Mastercard or Visa, because they invariably work on percentage-bsed MDRs (http://www.asiaconverge.com/2017/01/epayment-allows-govt-entities-to-cheat/).

- The RBI is silent on whether state government agencies with or without the involvement of private players like PayU.in can force a customer to pay the MDR. Normally, the merchant (the receiver of the money in exchange for goods and services) pays the MDR. Sadly, it is government agencies (with some exceptions like the income tax department and MTNL) which ask the customer to pay this fee.

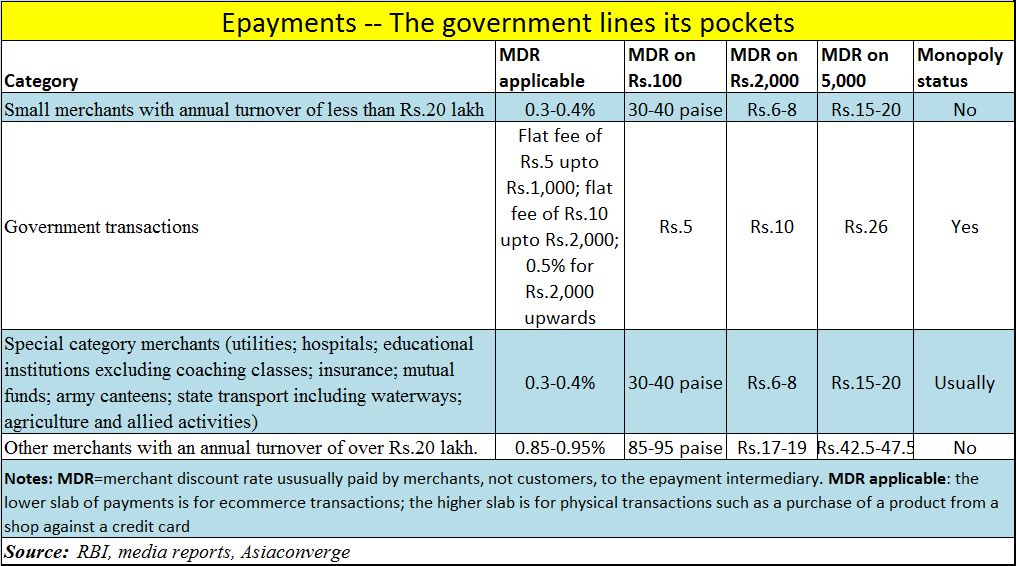

- In fact, since the government is a monopoly, hence accounts for huge volumes of transactions, it should be paying the lowest MDR. The RBI inverts this norm. The table shows government paying out the largest MDR (http://www.asiaconverge.com/2017/01/demonetisation-has-made-govt-richer-people-poorer/). This is both unfair and unwise.

- The best policies are those where all are put on an equal footing. The MDR for small transactions should invite a higher MDR (say 0.75%) while large value transactions could involve a lower MDR of 0.5%. This way, there is no need to create categories. All businesses would have to compete with the same rules.

- The RBI is silent on the commissions that payment gateways like PayTM should charge. Such entities charge no entry load. There are no commissions payable if a PayTM user pays to another PayTM user. But there is an exit load if the money is paid to a non-PayTM user. Since this is a rapidly growing sector, the RBI’s silence is baffling.

- The RBI is silent on the protocols that need to be followed by different players. The RBI must do this till a duly empowered regulator is put into place. It might be recalled that just recently there was a public spat between ICICI and YESbank. The latter was accused to not following the proper protocols. NPCI (National Payments Corporation of India) asked YESbank to honour the protocols, YESbank dismissed the request on the grounds that NPCI was not the designated authority for settling such matters. The RBI should have clarified its stand on such disputes.

In conclusion, it is good to see the government thinking about this sector. But it is sad to see the government coming up with bad ideas.

Clarification:

YESbank has stated that contrary to what was stated in #9 of the above PolicyWatch article, “there has been no communication or accusation from NPCI to YES BANK” with regards to protocols not being followed.

The author clarifies that the claim was based on a news item put out by All India Radio (see tweet at (https://twitter.com/airnewsalerts/status/822143117323210752 )

The author clarifies that the claim was based on a news item put out by All India Radio (see tweet at (https://twitter.com/airnewsalerts/status/822143117323210752 )

Also, YESbank has stated that it has not questioned NPCI’s authority as a regulator. It must be clarified that the challenge to NPCI was issued by PhonePE, not YESbank

However, it must also be noted that PhonePe is Yesbank’s epayments partner (https://www.yesbank.in/media/press-releases/fy-2016-17/say-goodbye-to-cash-phonepe-yes-bank-launch-indias-first-upi-based-payments-app). The author stands corrected on this score.

{kind=link}

COMMENTS