http://www.freepressjournal.in/analysis/rn-bhaskar-can-psus-help-improve-governments-balance-sheet/1081627

Can the government’s balance sheet be improved through revaluing PSUs?

The government is caught between a rock and a hard place. It wants to create jobs through massive spending on infrastructure. But for that it will have to spend money that it does not have (and FDI into infrastructure hasn’t taken off). This in turn means that it will have to go in for borrowing or raising resources through PSU disinvestment.

But debt is problematic. It is already a mill-stone weighing down public finances. It also prevents the government from getting a better credit rating. A poor rating prevents the government from gaining access to cheap international funds. There is the additional problem of the government having to service debt through interest payments. The higher the amount paid each year as interest charges, the greater is the probability of revenues being squeezed out, leaving little for developmental expenses.

But debt is problematic. It is already a mill-stone weighing down public finances. It also prevents the government from getting a better credit rating. A poor rating prevents the government from gaining access to cheap international funds. There is the additional problem of the government having to service debt through interest payments. The higher the amount paid each year as interest charges, the greater is the probability of revenues being squeezed out, leaving little for developmental expenses.

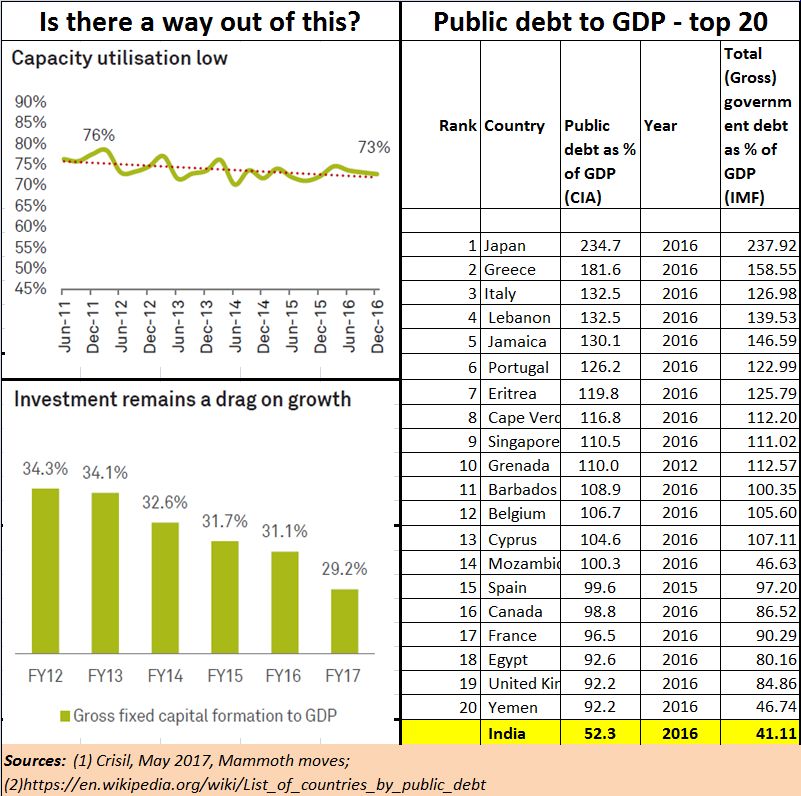

Actually, India’s debt is not large compared to many other countries (see chart). But when debt has the company of low investment, and low productivity, then problems multiply. Can money be freed for development purposes?

According to some, the way to do this is by taking a fresh look at valuing public sector units (PSUs). It is similar to the valuation exercise that was done during the ’nineties. It is similar to what has been recommended for banks (http://www.asiaconverge.com/2017/06/another-way-to-deal-withnpas-of-banks/). The PSUs are put through an exercise where they revalue and realise the full value of their assets by transferring them to respective subsidiaries. The revaluation of land is done transparently by using the ready reckoner rates put out by the income tax department.

As Pradip R. Shroff, a leading merchant banker explains, “In the present scenario, PSU disinvestment is popularly known as Reduction in Percentage of Equity Holding of Government of India (GOI) in PSUs including nationalised banks. Through the process of disinvestments, GOI gets one of the Sources of Funds for budgetary proposals/appropriations. The issue of additional equity shares by PSUs is another mode of Reduction in % of Holding of GOI in PSUs. In the latter case, the additional funds can only be used by the PSUs and do not go to the government (2017-06-08_PSU-strategy-Pradip-R-Shroff-note.doc).”

Äs most economists also explain, the ultimate Concept of PSU Disinvestment results in raising Long Term Resources of Funds, which neither carries any repayment burden nor any interest burden. This is what the government did when it began the PSU disinvestment programme during 1991-1992 and continued with this strategy thereafter.

Investment bankers, like Shroff, believe that there is a need to take a re-look at PSU disinvestments from a different angle. And this is what they propose:

- The detailed study of Shareholding Pattern of PSU Undertakings (see 2017-06-08_PSU-strategy-P-R-Shroff-supporting-datasheets.pdf) reveal that the shares of most PSUs are held by government owned insurance companies like LIC and nationalised banks. But at times PSUs also hold a good share of equity in other PSUs. These holdings become part of their respective investment portfolios.

- It would be a good idea for the government to propose to the RBI and the Parliament that additional investments by way of subscription to equity shares of PSU Undertakings by banks should be considered as SLR grade. SLR refers to statutory liquidity ratios that banks must maintain by investing in government approved securities (https://www.rbi.org.in/Scripts/BS_CircularIndexDisplay.aspx?Id=10640). This way, banks are permitted to subscribe to the additional PSU shares issued. Banks meet their SLR norms. The PSUs get the funds they require without dilution of government holding.

- The government could also consider issuing additional equity shares of PSUs to non-resident Indians (NRIs) through ADRs (American depositary receipts, which are negotiable certificates issued by US banks and represent a specified number of shares (or one share) in a foreign stock traded on a U.S. exchange). This will permit PSU shares to get quoted in foreign exchange as well. Typically, the ADR price more or less reflects the Indian rupee equivalent of the total value of equity shares of the same company quoted on Indian exchanges.

- A study shows that the market capitalisation of GOI in PSUs (other than nationalised banks) is approximately Rs.1,559,377 crore which equals to $ 24,046 crore (or $240 billion) at an exchange rate of Rs.64.85 to a US$ (see document 2017-06-08_PSU-strategy-P-R-Shroff-supporting-datasheets.pdf).

- The GOI holding in nationalised banks is Rs.291,161 crore which equals $ 4,490 crore (or US$ 45 billion).

- Investment bankers are confident that if IMF and the World Bank are approached, they may not be averse to consider at least 50% of $ 285 billion ($ 24046 + $ 4490 crore) as equivalent gold reserves. That would boost India’s equivalent gold reserves by US$ 142.68 billion (see 2017-06-08_PSU-strategy-P-R-Shroff-supporting-datasheets.pdf).

- Such a move could improve India’s credit rating, and also get it an additional cushion of forex reserves (2017-06-08_PSU-strategy-Pradip-R-Shroff-note.doc).

That could leave the government with additional funds to invest on infrastructure, to create jobs and to kickstart the economy.

But all this is a mere accounting exercise. To make this work, the government needs to focus on governance, credible judicial processes, and sensible economic policies. Otherwise, corruption (URL) will erode benefits, and a sense of well-being could tempt the government to more profligacy. Remember how political compulsions compelled even the present ruling party to allow for loan waivers in Uttar Pradesh? It has now to re-educate the rest of India why loan waivers are bad in principle.

Simultaneously, there is the urgent need to stanch losses from unproductive PSUs.

There is also the critical need to penalise legislators and bureaucrats who sometimes allow PSUs to become sick, so that they could be allowed to be taken over by private interests (Air India fits this bill).

Respect for corporate governance is therefore the key. If the government wants to save India, this is what needs to be focused on first.

{kind=link}

COMMENTS