Source: http://www.moneycontrol.com/news/business/economy/comment-dont-entrust-the-fate-of-banks-to-the-government-2477915.html

Should you trust the government with banks?

The banks lent out money irresponsibly because India’s politicians in power thought that they could use the banks to win favours from industrialists.

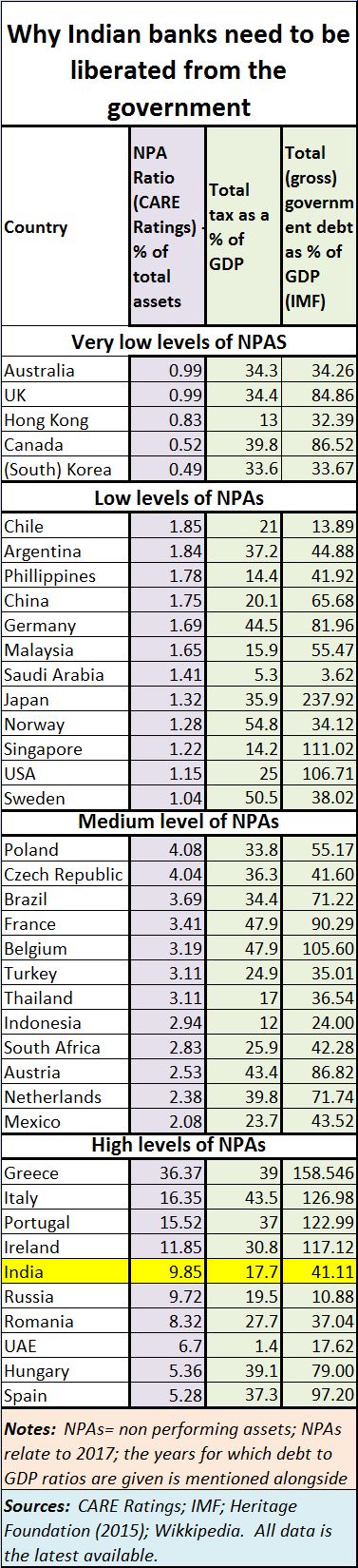

Ideally, countries should have a low NPA ratio, a debt-to-GDP figure of around 50%, and a tax-to-GDP number of around 30-50%. When one of these numbers go out of sync, someone should be asking why.

Let us take Saudi Arabia’s example. It has a very low tax-to-GDP figure. But that is because the government had huge amounts of money through the sale of oil. It became largely a welfare state. The other two ratios are excellent. Now with oil prices falling, there is a good possibility that the government may decide to push up the tax-to-GDP ratio.

Let us take Saudi Arabia’s example. It has a very low tax-to-GDP figure. But that is because the government had huge amounts of money through the sale of oil. It became largely a welfare state. The other two ratios are excellent. Now with oil prices falling, there is a good possibility that the government may decide to push up the tax-to-GDP ratio.

Similarly, look at the UAE. Its NPAs are high, quite atypical of an oil exporting country. But that could be also because Dubai suffered a huge reversal during the financial meltdown in 2008. That was when Abu Dhabi had to bail it out. Huge exposures to real estate and gold speculation caused its banks to fail. Like Saudi Arabia, it is largely a welfare state, and does not depend on taxes. However, with falling oil revenues, Dubai has just decided to levy a VAT on all its products. Expect this number to go up in the next two years.

Good countries allow themselves to have higher debt-to-GDP numbers. But they do not erode the sanctity of banks.

What about India?

India’s numbers also tell a story. Its NPAs are high because of irresponsible lending by banks. But why blame banks alone? The banks lent out money irresponsibly because India’s politicians in power thought that they could use the banks to win favours from industrialists. What favours could politicians want from industrialists? Kickbacks is a good possibility. Election funding is another.

That could also explain the reluctance of investigators going after politicians. They have at best begun investigating bankers.

Remember the fate of Telgi investigation? Remember how television networks aired a confession by Telgi implicating a politician behind the scam? That politician is being investigated for other crimes but not the Telgi scam which dealt with government paper – akin to treasury notes.

The politician is also supposed to have pushed for auctioning of police promotions and lucrative postings to the highest bidder. A former police commissioner had written articles about this in leading media publications. But that matter too is not being investigated. Similarly, expect the banker-politician nexus to remain unexposed.

But then Indian banks have a history of bailing out governments.

It may be worth recalling that the formation of Imperial Bank, now the State Bank of India, was itself the result of near bankruptcy. This is something that Ameya Bagchi brings out quite lucidly in his book ‘History of the State Bank of India’. He talks about how the East India Company set up the Bank of Calcutta to garner deposits which were used to finance wars that Lord Wellesley waged against ‘upstart’ kingdoms. But wars cost money and soon Bank of Calcutta was on the verge of bankruptcy. So, East India Company started a bank in Chennai – the Bank of Madras, which offered a slightly higher rate of interest than Bank of Calcutta because more money was needed to finance the wars.

What it did not expect was that the wealthy Calcutta Marwaris would immediately relocate themselves and transfer their funds to the Bank of Madras where they could benefit from the higher deposit rate. Bank of Madras used its money for financing these non-productive wars.

Finally, the British Crown had to step in and bail out these banks by merging the Bank of Bombay, Bank of Calcutta and Bank of Madras and forming the Imperial Bank, and then making its government run. When it became the State Bank of India, the British Government’s shares went to the Indian government and the bank remained a government controlled company though some shares remained in the market and were listed on stock exchanges.

But the systems the British government put in place ensured that this bank would remain one of the best government-controlled banks. It refused to centralise decision making, and hence it was difficult for governments to push an individual into clearing reckless loans. That was not the case with other State Banks which were amalgamated into SBI through the SBI (Subsidiary Bank’s) Act. Seven other state banks became subsidiaries of the SBI, hence government-controlled.

But the bigger blows to Indian banking were to come in 1969 and in 1984. Former Prime Minister Indira Gandhi decided to nationalise 14 banks in 1969. The stated reason was that banks had to become more relevant to rural India and to the needs of the common man. But the nationalisation of Syndicate Bank debunks this pious myth. This bank grew from collecting just 25 paise (Pigmy) deposits from poor people. It was the only bank to have its headquarters in (then) rural Manipal and catered largely to rural needs. This showed that the motive of nationalisation was not the farmers’ interests. Indira Gandhi wanted to cut the purse-strings of industries and wanted to control both banks and industrial licences.

An unfortunate episode of 1971 known as the Nagarwala Case also seemed to point to the possibility of politicians dipping into banks funds. The case was never fully investigated and Nagarwala died in custody.

But the biggest blow to banking came in 1984 when the government under Indira Gandhi decided to give away money to rural folk without collateral. Her finance minister Janardhan Poojary announced the Loan Mela scheme which allowed people to borrow upto Rs.1,500 per head without collateral. Everyone knew that they money would never come back. The age of loan waivers had begun. Banks were doomed.

None of the amalgamated stated banks and the nationalised banks had the banking culture and the checks and controls that SBI had. No wonder, these banks accounted for the largest share of non-performing assets. Each of these banks had been ‘persuaded’ to give loans to favoured industrialists, often without even a proper feasibility study being done. How else does one explain Rs.40,000 crore being given away to Bhushan Steel or over Rs.1.4 lakh crore being given away to the Ruias of Essar. Clearly, the game of favourites was still being played out.

Fortunately, the present government is now determined to cleanse the books. It has refused to allow bad accounts to get concealed through ever-greening (where the borrower takes additional money from the banks and pays the interest from these additional funds and hence does not remain a defaulter). So industrialists are being hauled up. Some bankers are being investigated. But the politicians who asked the banker to lend the money still remain scot free.

The NPAs could be bigger

In fact, India’s NPAs could be bigger if cooperative banks are also taken into account. These are banks which are supposed to be overlooked by state governments. In Maharashtra (and possibly in other states as well), even the 10% of a bank’s funds known as promoter’s contribution, is put in by the state. This is done without the state even insisting on a government-appointed director to be on the board of the cooperative banks. Thus the board is filled with appointees of people close to politicians. They collect money from poor folk and lend it out to people with clout. They often do not even recover the money lent out. Very convenient, isn’t it?

The best documented case of such happenings is that of Maharashtra State Cooperative Bank (MSCB) which saw its board dissolved in May 2011. This came on the heels of reports from Nabard (which put the losses at Rs776 crore only during 2009-10). MSCB’s total net worth had been wiped off and it was in the red by another Rs.140 crore. NPAs were estimated to be in the region of 30%. Nabard sent its report to the Reserve Bank of India (RBI) which informed the state government, which in turn decided to allow for the board being dissolved. With new government-appointed administrators, the bank began making healthy profits within three years.

The RBI has data relating to the functioning of all cooperative banks. But it will not make this data public because it says that these banks are governed by state governments. But the money comes from tax payers and common depositors. Protecting depositors and cleaning up all banking is the RBI’s job. Not disclosing this information is therefore injurious to the banking culture and environment.

Should government be trusted with banks?

The RBI’s refusal to come up with data relating to cooperative banks; its reluctance to disclose names of defaulting groups (till the Supreme Court had to nudge it to begin disclosures), and the silence on the part of the government and the RBI about politicians who gave the order to bankers makes one wonder if the government should be trusted with banks at all.

The RBI needs to be empowered to disclose all instances of default, including those by cooperative banks.

The government should investigate further and come up with the names of politicians who persuaded bankers to remove their hands from the cash till.

And, more importantly, the courts need to come out with guidelines on how to deal with loans waivers (since neither the RBI or the legislators have to date). This is crucial because in Maharashtra, the loan waiver to farmers may become an albatross around the already burdened banks. Last fortnight, the government asked banks to take a haircut on loans advanced to farmers.

If a haircut has to be taken, it should be added to the state’s budget. It is not to be added to a bank’s NPA basket. That would be stealing Peter to pay Paul. It is stealing, nothing less. And this is where we need to go back to the chart. India has a low debt-to-GDP number. But that is also because the government has constantly found ways to transfer some of its debt to the banks, or get it concealed through court disputes.

India likes to show that it is a prudent borrower. But that is because much of the political funding and graft comes through loans given out to banks, or through loan waivers. Each government has resorted to loan waivers, throwing prudence to the winds.

Even the current government tried to push back the practice of loan waivers. But it chose to succumb to political demands and allowed a loan waiver in UP. That snowballed into similar demands from other states, notably Maharashtra, Gujarat and Madhya Pradesh. Now the government wants banks to take a haircut!

The amount of loan waiver should either be met out of political party funds or added to the state balance sheet. Please don’t mess around with banks.

Banks are, after all, the most visible symbol of good business practices. When this is destroyed, all business practices will suffer. Costs will go up because disputes and litigations too have a cost that companies pass on to customers.

True, passing on such NPAs to the state budget will burden innocent tax payers. But that is better because the state’s taxes come largely through indirect taxes which are paid by everybody, including rich farmers who benefit from tax-free agricultural income disclosures (http://www.asiaconverge.com/2016/07/indias-biggest-laundromat-agriculture/). Bank deposits usually relate to relatively law abiding tax-paying people. Burdening them once again is not fair. The government’s refusal to tax agriculture has allowed the tax-to-GDP ratio to remain among the lowest in the world.

Yes deposit insurance needs to be increased from Rs. 1 lakh to at least Rs.50 lakh (that is the money pensioners sometimes keep with banks). But arming the government with powers to use depositors’ money to bail out cash-strapped banks is not the right way. True, there may be safeguards. But why have the clause at all? Past experience shows that the government cannot be trusted with managing banks. Arming it with additional powers will harm banking and depositors even more.

{kind=link}

COMMENTS