http://www.freepressjournal.in/analysis/bank-mergers-abracadabra-mess-vanishes-r-n-bhaskar/1363483

Bank mergers, LIC and IL&FS: abracadabra! See the mess has disappeared!

— By | Sep 27, 2018

There is trouble that is bubbling inside India’s financial cauldron. The three witches cackle, stir their brooms in the broth, and chant incantations that make the weak and the credulous sit up with open-mouthed wonder. Sceptics sit some distance away. They shake their heads. They know that little good could come of this exercise.

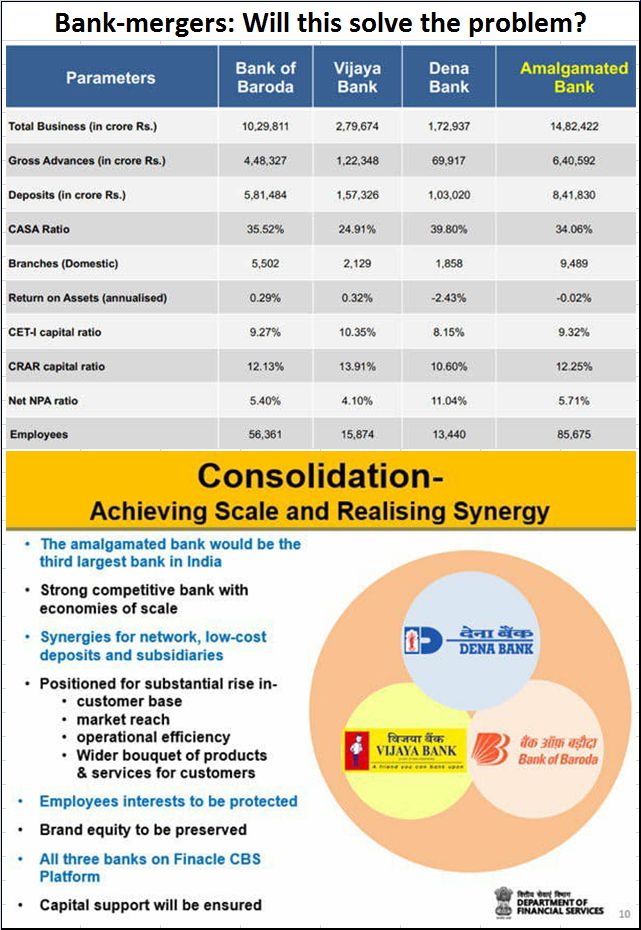

Yes, you do have the best of rating agencies praising the merger of three banks – Bank of Baroda, Vijaya Bank and Dena Bank (https://www.indiaratings.co.in/PressRelease?pressReleaseID=34000&title=proposed-amalgamation-of-bank-of-baroda-vijaya-dena%3A-long-ended-benefits%2C-though-near-term-challenges). The reasoning is right (see chart alongside); the numbers seem okay; but there is a growing sense of discomfort. How can one wish away the causes that led banks to this juncture by brushing them under the proverbial carpet?.

Yes, you do have the best of rating agencies praising the merger of three banks – Bank of Baroda, Vijaya Bank and Dena Bank (https://www.indiaratings.co.in/PressRelease?pressReleaseID=34000&title=proposed-amalgamation-of-bank-of-baroda-vijaya-dena%3A-long-ended-benefits%2C-though-near-term-challenges). The reasoning is right (see chart alongside); the numbers seem okay; but there is a growing sense of discomfort. How can one wish away the causes that led banks to this juncture by brushing them under the proverbial carpet?.

Foremost among the causes is the growing incidence of bank fraud. As these columns had pointed out recently (http://www.asiaconverge.com/2018/08/banker-scams-ter-and-visible-hand-make-merry/) even the government admitted to this before the Lok Sabha on 3 August this year – just a month before the three banks were merged.

The government pointed out that over a period of just five years, Indian banks registered 24,584 cases of fraud, involving a mind-boggling sum of Rs.1.04 lakh crore, Sadly, both the number of cases of fraud and the amounts involved kept on growing year after year. During 2017-18 alone, the banks had registered 5,879 instances of fraud involving Rs.32,048.65 crore.

You cannot expect the banks to become good if the guilty are not punished. Yet, the government in its incredible wisdom decided not to allow investigation agencies to query or prosecute any banker till permission for doing so was sought from the higher-ups (http://www.asiaconverge.com/2018/08/india-passes-the-promotion-of-corruption-act/). The government did this through suitable amendments to the Prevention Of Corruption Act. Since it is reasonable to expect the higher-ups to be in collusion with fraudsters, it is unlikely that such consent will be forthcoming, unless of course the banker has fallen foul of the senior-most of politicians and bureaucrats (http://www.asiaconverge.com/2018/08/banker-scams-ter-and-visible-hand-make-merry/).

With no provision for weeding out (a) the undesirables, and (b) the excess fat, it is not clear how the just-merged-entity will be able to become a healthy vibrant bank capable of facing the financial headwinds that are only going to get fiercer.

Take the second sleight of hand. IDBI has been taken – kicking and screaming – to be merged with LIC (Life Insurance Corporation). And now the government wants IL&FS also to be taken over by LIC.

That gives rise to several issues. Yes, LIC has the financial muscle to take over the losses of IDBI and IL&FS. But remember that both these entities are not shares that LIC picks up from the markets, holds on to them, and then sells them when the time is right. Both IDBI and IL&FS are running businesses, whose cultures do not match those of LIC.

LIC is into life insurance – and it must focus on very long-term investments and maturities. That compels it to be extremely risk averse. Suddenly, you club it with IDBI which is a bank with an appetite for mid-level risks and returns. IDBI is also saddled with some people who have learnt to defraud the bank (and its customers). It is an organisation which appears to have forgotten how to even send out SMS alerts to customers even after charging them. Will LIC be given the powers, and will it have the skill, to cleanse it of the rot?

Then take IL&FS. Remember Maytas? It was part of the infamous Satyam group, and held some of the largest land-banks which are believed to be owned in partnership with very powerful people. IL&FS fought hard to take over this company. It understands land-banks. It deals with high-risk-high-reward lines of businesses. A recent FPJ report showed (http://www.freepressjournal.in/business/ilfs-crisis-road-leading-to-dead-end/1359180), IL&FS has at least “24 direct subsidiaries, 135 indirect subsidiaries, six joint ventures (50:50 equity ownership) and four associate ventures (varying degrees of equity ownership)”. Also, typically, the senior management at project level has more ex-IAS people than most similar companies. It is a pattern lending itself more to efficient liaison rather than efficient infra project execution. Can LIC handle a hot potato like IL&FS which carries it with the contagion of projects where high level wheelings and dealings are involved? Or could it be that the government is itself interested in retaining control over the landbanks and the payouts through the innumerable subsidiaries?

It is these developments which make even the hardnosed watcher of financial markets a bit nervous. The protection to bankers is the last thing that was wanted at this time. Getting bank unions to work with policy makers was urgently needed. In the absence of both, there could be a lot of bubble and trouble ahead.

{kind=link}

COMMENTS