https://www.freepressjournal.in/business/policy-watch-e-solutions-cannot-substitute-efficiency-integrity-and-intelligence

India stunts its own ecommerce potential

RN Bhaskar

India has always prided itself on its IT (information Technology) skills. It believes that it can become the world’s outsourcing hub for technology.

It believes that it could become the biggest ecommerce and esolutions market in the world. Hah!

It allows transactions to take place within a fraction of a second but takes months or even years to register or resolve disputes related to such complaints. There is as yet no regulator for ecommerce.

It allows transactions to take place within a fraction of a second but takes months or even years to register or resolve disputes related to such complaints. There is as yet no regulator for ecommerce.

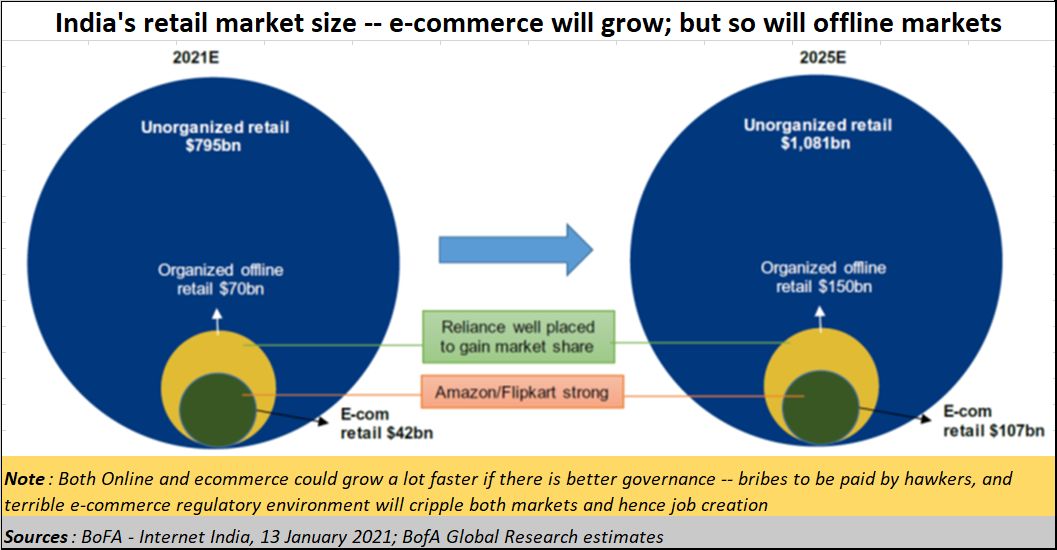

The market could be bigger – maybe bigger than even the Chinese market, if only there were good regulation and governance. But with little hope for effective and speedy dispute resolution, ecommerce is still viewed with great suspicion. Local owners of brick-and-mortar establishments are happy that ecommerce will be stumped. But they fail to realise that both the offline and the online markets could be a lot more vibrant had there been better governance.

In the offline market, the problems of hawkers and resultant bribery is common folklore by now in almost all parts of India (http://www.asiaconverge.com/2017/12/solution-indias-parking-hawker-problem-kills-graft-rewards-investors-unclutters-roads/).

When it comes to IT, the problems are bigger. Look closely. Many of these problems relate to efficiency, integrity, and intelligence. Governments at both at the centre and in states do not like talking about this.

True, governments have been falling over each other to show people that they have become both IT savvy and are IT friendly. Websites are being spruced up. The favourite buzzword is having an app. Government officials think that having an app will be a good solution to most problems. There is an app for police complaints, an app for railways complaints too. But, as always, it is a case of GIGO – garbage in, garbage out.

So, you have the CEO of NITI Aayog appearing at prime time on television explaining how the Aarogya Setu has become the most popular download almost immediately after it was introduced. When it was found that it was riddled with leakages, and security flaws, it became nobody’s child. Global security experts warned of major security flaws in the app. It soon became a hot potato. Nowadays, responses to RTI (Right to Information) applications show that nobody even knows who created the app (https://www.newsclick.in/veil-secrecy-RTI-aarogya-setu-drawn-blank-reveals-Rs-4.15-cr-spent-publicity).

RTI enquiries also show that hefty payments had been made to people who were apparently connected with the creation of Aarogya Setu. But none of this is confirmed by the government. Integrity, intelligence, and efficiency are all involved. The country’s standing in the IT world has sunk a bit lower.

Ditto with the CoWIN App for Covid-19 vaccine registration. The app crashed during the first couple of days of the vaccination drive. Why should any website crash, or any app malfunction? Is this mismanagement, or just a case of awarding the work to people who were inept at their jobs?

Ditto with the CoWIN App for Covid-19 vaccine registration. The app crashed during the first couple of days of the vaccination drive. Why should any website crash, or any app malfunction? Is this mismanagement, or just a case of awarding the work to people who were inept at their jobs?

Hence, you have servers for college examinations that are known to crash. So do websites dealing with school or college admissions.

Year after year, the website for the ministry of corporate affairs (MCA) the GST or Income Tax crashes. That is not a flattering picture of a country that claims it could be the IT hub for the world.

The website of the richest municipality in India, the MCGM (Municipal Corporation for greater Mumbai), does not work well for epayments. It is a newly designed website, introduced even while the earlier one was working well. Looks like nobody told them of the saying, ‘Don’t try fixing something if it ain’t broke’. Consumers have complained about the non-functioning of the payment portal for water and property taxes. The problem, we are told, is being looked into.

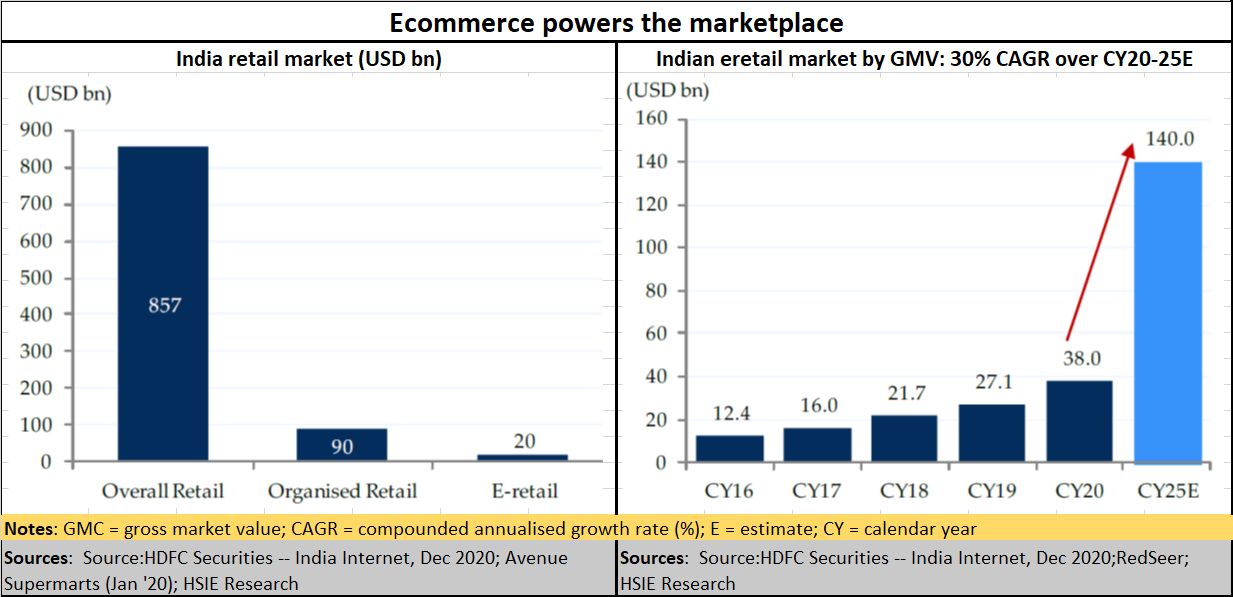

Little do the state’s policy makers realise that the potential for ecommerce growth is huge (see chart). They are just killing it with sloth or collusive deals.

Police capabilities

The police website in Mumbai looks good till you start using it. The OTP for registering online complaints does not arrive. Emails about this problem have been sent to the police commissioner, but the problem has not been rectified. This author has tried this several times, but with no luck.

The police department’s way of showing that law and order situation has improved is to discourage any filing of complai8nts. Go to most police stations, especially in the suburbs. You are asked to wait for a couple of hours till a complaint is written out, that too reluctantly. The cops tell complainants how overworked they are and try making them feel guilty about filing complaints. That is why the police department does not like ecomplaints. It therefore invents ways to prevent ecomplaints as well (a peek at the twitter chain can be quite educative here — https://twitter.com/rnbhaskar1/status/1355129239234879492?s=20). Emailed complaints (the best way for the disabled and senior citizens to register complaints) are often ignored by many deputy municipal commissioners after the police headquarters forwards these complaints to them.

Then there are collusive deals as well. Earlier the MCGM’s website had tied up with a payment gateway which added a surcharge on all bills, but the amount was not mentioned on receipts (http://www.asiaconverge.com/2017/04/mcgm-epayments-point-to-dangers-of-epayment/). A police com plaint was also registered. But the MCGM’s glib reply was that MCGM was not taking the payment. “The payment is reflected in your bank debit,” said the MCGM officials. “It is being charged by the payment gateway.” IRCTC and other government departments showed this amount on the receipts. The MCGM probably had off-the-books arrangements with the payment gateway.

Scams galore

Still earlier, a banking software allowed letters of understanding (LOUs) to be issued without getting reflected in the central registry (http://www.asiaconverge.com/2018/02/pnb-why-did-the-dogs-not-bark/). The software developers had either forgotten to look at the loophole or had colluded with the authorities. This was the loophole used by Nirav Modi to draw out money on fake LoUs from several banks. Harshad Mehta had done the same thing with fake Bankers’ Receipts (BRs).

The scene of crime changed. But the modus operandi did not. Curiously, neither has the application developer been hauled up, nor has any case on the malfunctioning of the banking software been registered.

A similar gap was left uncovered when NSEL was found to be trading in stocks that did not exist in the warehouses at all (http://www.asiaconverge.com/2014/06/auction-off-nsel-defaulters-assets-restore-investor-confidence/).

All the instances above show that governments – both at the state and the central level – have been creating clever schemes to either defraud common citizens or dump them with IT solutions that do not work. Someone pays the developers hefty fees for the apps and website services that do not deliver. And since they are government or quasi-government solutions, the actual burden is borne by taxpayers.

Yet, and one can be reasonably sure about this, no police case has been registered for the failure to deliver a fully functioning app, even though payments have been made. This could also be because most corruption cases against prominent politicians have been closed for want of evidence.

Welcome to a Brave New India, where IT excellence is now becoming more of a rarity. This is because shortcuts are being encouraged or adopted for a variety of reasons. And all this is happening when global ecommerce markets are booming.

Bank KYC

Then there are other areas where there is an utter lack of understanding about how information is to be used. Take Bank KYC (Know Your Customer) norms for corporate account holders.

The bank gives you a whole list of documents that are required about the company — the Memorandum of Articles, its Memorandum of Association, names of its directors, Aadhaar cards, PAN cards, passport copies etc. The bank wants all the papers signed with the company’s rubber seal also affixed. The sad part is that all these documents are already there with the Ministry of Corporate affairs (MCA). Go to the MCA website and each and every bit of information is available there and is updated each year.

All companies have PAN cards, and these numbers are linked to the corporate unique identify (UID) and to the directors as well. The banks have the PAN card details – submitted at the time of opening the account — and details of the UID. All they had to do was to link this to the MCA website.

But no! They want documents, which must be studied by auditors at the bank’s headquarters. If the stamp is missing the documents are returned. Can the RBI, the government and the banks not resolve this without wasting paper, customers’ time and expending the energies of harried employees of the banks themselves? A total abdication of common sense and good practices is in evidence.

No wonder then that most people are vexed with the way banks function and the way KYC works (https://www.moneylife.in/article/should-non-kyc-complied-bank-account-holder-be-penalised/35964.html). Yes, all the guys at the government’s planning cells, the RBI and the banks have heard of electronic databases, ecommerce, and ebusiness, but have shown utter reluctance to use them sensibly.

At the heart of the KYC is the Aadhaar card. This author had his KYC form rejected twice because the auditors at the central office complained that the photograph was not clear. The original Aadhaar card was shown to the bank and it was confirmed that even the original did not have a clear photograph. Copies of the passport pages were submitted instead, where the photograph was visible. The auditors insisted on an Aadhaar card. Finally, the auditors relented when it was pointed out that the passport was certified by the President of India, while the Aadhaar was not. That settled the issue. Once again, basic common sense was missing.

At the heart of the KYC is the Aadhaar card. This author had his KYC form rejected twice because the auditors at the central office complained that the photograph was not clear. The original Aadhaar card was shown to the bank and it was confirmed that even the original did not have a clear photograph. Copies of the passport pages were submitted instead, where the photograph was visible. The auditors insisted on an Aadhaar card. Finally, the auditors relented when it was pointed out that the passport was certified by the President of India, while the Aadhaar was not. That settled the issue. Once again, basic common sense was missing.

But there is a more serious issue. The government wants KYC to prevent frauds when the Aadhaar card itself could be the cause of many frauds. By allowing (even insisting) that the Aadhaar card be the sole document on the basis of which PAN cards can be issued the government has opened a window to one of the biggest money laundering opportunities in India (http://www.asiaconverge.com/2020/11/double-vision-of-rbi/).

Regulatory issues

Then there is the regulatory problem.

To date, neither the government, nor the RBI has clarified whether Google Pay is a licensed player or not. It is one of the most popular payment apps in the markets in India. But Google Pay is not listed among those cleared by the RBI for epayment, ecommerce and other such activities as of January 5, 2021 (https://www.rbi.org.in/scripts/publicationsview.aspx?id=12043). Yet Google Pay continues to operate in the financial markets in India. So, is it an unregulated player? Are such players permitted? Why is everyone quiet about this? (http://www.asiaconverge.com/2021/01/the-alibaba-episode-has-lessons-for-ecommerce-in-india/).

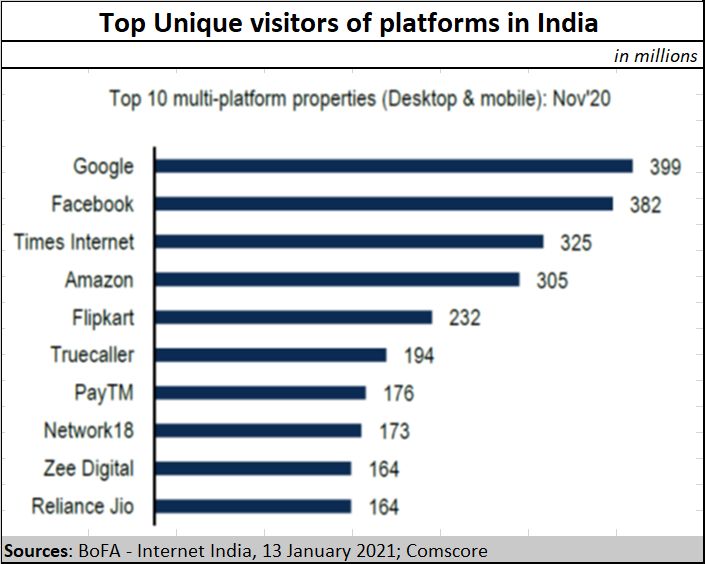

Thus, even though there is a surge in unique visitors to various platforms in India, there is a lot of skittishness as well. Nobody is sure any more about who is legal and who is not.

This is a big concern because it has a lot to do with the selective approach to laws. The moment Amazon approached the Singapore Arbitration Courts and got a stay on the deal that the Future group plans entering into with the Reliance group, it has been targeted for FDI violations, irregular contracts (https://timesofindia.indiatimes.com/business/india-business/centre-directs-ed-rbi-to-act-against-amazon-flipkart-for-fdi-fema-violations/articleshow/80043646.cms) and even streaming shows that shows that ‘hurt’ Indian sensibilities.

Maybe, this could be sheer coincidence. But such coincidences have been happening a bit too often. As a result, a feeling of discomfort keeps growing. You cannot have a healthy ecommerce environment if laws are to be applied selectively, and if there is no clarity on what is legal or otherwise.

But this type of transparency is something the government has not even cared to address, though it does pay a lot of lip service to such claims. The issues listed above are just the tip of the iceberg. The blatant disregard that the government shows towards disclosure can be seen from the way it refuses to share even Lok Sabha and Rajya Sabha answers with the public. Yes, they seem to be there on the government websites, but they are not easy to access any more. You cannot locate them by using search engines, the way one could earlier. You now need to know the session number, the date and question number etc. to retrieve the answers. Tables and annexures that come with these replies are even more difficult to come by.

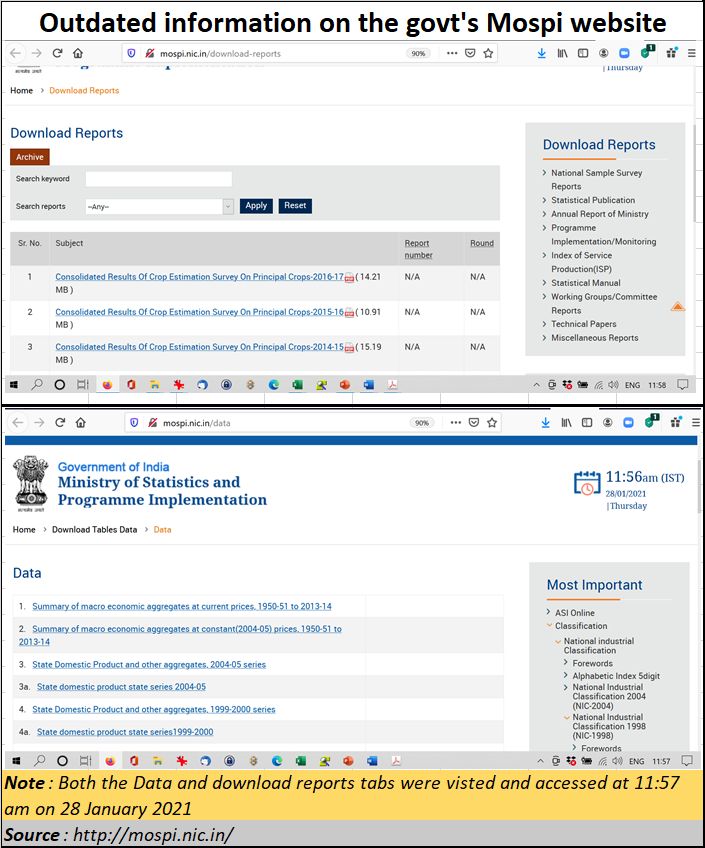

Look at the screenshots alongside. They relate to the ministry of statistics and programme implementation (Mospi). We just looked up the pages on ‘data’ and ‘download reports’. The data and reports listed there are for 2013-14, and 1950, As for the state GSDP and the data stops at 2015-16. This does not tell the story of an India that is computer savvy, that has all the information that is required at its fingertips.

Look at the screenshots alongside. They relate to the ministry of statistics and programme implementation (Mospi). We just looked up the pages on ‘data’ and ‘download reports’. The data and reports listed there are for 2013-14, and 1950, As for the state GSDP and the data stops at 2015-16. This does not tell the story of an India that is computer savvy, that has all the information that is required at its fingertips.

Governance and transparency begin with the provision of data. Not granting people free access to economic or social information is the starting point of corrosion and corruption.

{kind=link}

COMMENTS