INVESTMENT PERSPECTIVES

By J Mulraj

Mar 4-10, 2023

The perils of shareholder capitalism

The GINI coefficient is a way to determine how equal a society is, in terms of income distribution. The higher a country’s rating on the GINI index, the more unequally its income is distributed. The top ten countries with the highest GINI coefficients (most unequal) and the bottom 10 (least unequal) are given here (https://worldpopulationreview.com/country-rankings/gini-coefficient-by-country). Its interesting to see that 4/5 most unequal countries are in Africa and 5/5 of of the least unequal are former Soviet Union countries. India’s GINI coefficient is 35.7, below that of China 38.5 and USA 41.4.

Income inequality is one of the main reasons for conflict and geopolitical tensions. But can inequality be significantly reduced? Can a GINI be put back in the bottle?

Global income is about $ 108 trillion. It was just over $ 1 trillion two centuries ago. Along with growth in income came growth in stock markets. Before stock markets were established (the Amsterdam stock exchange was set up in 1611), capital was provided by the landed gentry and the nobility. The capital needed to finance a trading expedition was locked in for months, sometimes years, so the stock of capital dried up. The Dutch launched the stock exchange to allow the common man to fund these missions, in smaller tranches. The investor could exit, if needed, by selling his share to someone else, without disturbing the mission itself. Stock exchanges thus helped the common man, not just the landed gentry, to participate in economic growth, and get income.

Stock markets became a means to participate in the economic growth of countries, of course, through sensible investment practices. In the ‘80s Japan, and Germany, began catching up with USA, by following a form of capitalism, called stakeholder capitalism. In this, the company seeks to balance the interests of all stakeholders, viz. providers of capital, employees, customers and suppliers. This form of capitalism was successful and the Japanese stock market boomed, making investors wealthy. The most expensive stock in the world then was NTT DoCoMo, their telecom company. In 1989 Japanese Mitsubishi Estate bought Rockefeller Centre in NYC, and in 1990 Matsushita Electric of Japan bought Universal Studio of USA.

The US countered with shareholder capitalism, under which the interests of providers of capital gain primacy over those of other stakeholders. This form is more efficient than stakeholder capitalism, which is a more benign form, with a longer term approach. It worked, and the US regained its dominance, even as Japan went into a slump, economically as well as the stock market.

But shareholder capitalism created its own set of problems. One was a sharp focus on short term performance, to the detriment of long term development. An early example was Lucent Technologies, which was the font of innovation called Bell Labs, a division of AT&T before it was spun off as a separate company when AT&T (known as Mama Bell) was split into seven baby bells through a court order. The then management of Lucent cut capex on long term innovations in order to boost quarterly profits, keeping analysts happy and the stock high. But it lost its innovative edge and nearly went bankrupt.

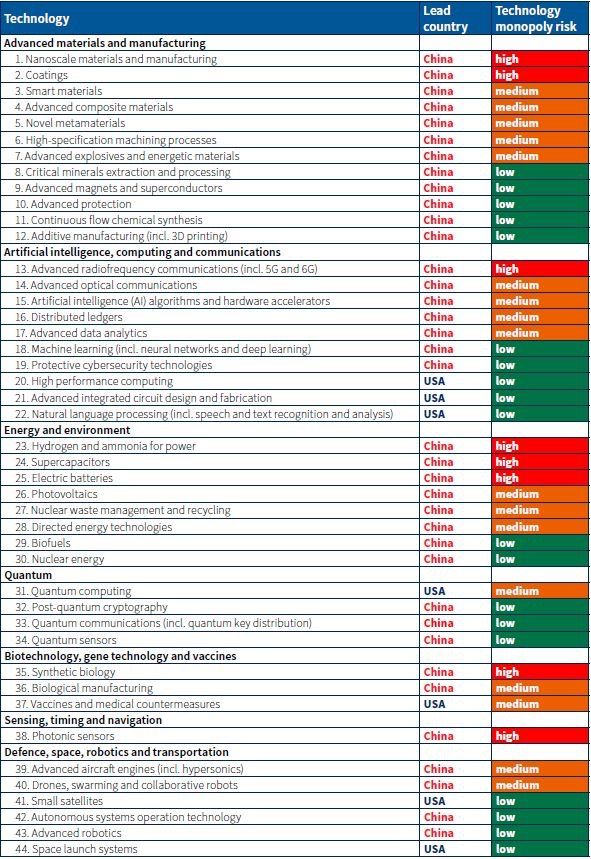

Fast forward to today. A study by the Australian Strategic Policy Institute, funded by USA, to determine whether China or USA was leading in 44 technologies, concluded that China is leading in 37/44. USA leads in only 7. The table below lists them.

A big reason for this is the focus on short term profit by US corporate management, practicing shareholder capitalism, sacrificing long term developments. Chinese companies, directed and funded by the State, can, and do, focus on the long term.

A big reason for this is the focus on short term profit by US corporate management, practicing shareholder capitalism, sacrificing long term developments. Chinese companies, directed and funded by the State, can, and do, focus on the long term.

The winner of the technology race will be the leading economy in the Fourth Industrial Revolution. The First, in 1784, developed the use of steam and mechanical power. The Second, in 1870, developed mass production. The Third, in 1969, was led by electronics, IT, and automated production. The Fourth will focus on new technologies such as AI, 5G, Quantum Computing, autonomous vehicles, and others.

So this weakness of shareholder capitalism would need to be addressed. Else the US will lose its role as the economic hegemon.

Another weakness is the geographical spreading of supply chains, in order to improve efficiencies, lower cost of manufacture and boost profits, which is the aim of shareholder capitalism. The advent of Covid brought out the vulnerabilities of the western world to an extended supply chain. The most recent impact, for USA, is in the burgeoning auto debt. It was the shortage of electronic chips, due to supply chain disruptions during Covid, that led to a spurt in prices of second hand cars, and a bank funded demand for them. This has now collapsed, also thanks to rising cost of bank loans. Auto loan debt, at over $ 1.5 trillion, can trigger a default, just as the sub prime mortgage loan crisis triggered a meltdown in 2008. Driven by the need to better shareholder returns, banks had, then, given sub prime loans (by definition, loans to borrowers who did not qualify), securitized the loans and sold them to investors seeking a higher return, and trusting credit rating agencies which rated them safe! Today, the crisis is auto loans. Fun fact: This paper estimates the potential loss of subprime loans then, at $ 420 b. The auto loan outstanding is $ 1.5 trillion!

One of the outcomes of shareholder capitalism was the growth of the US mutual fund industry, which now controls more financial assets under management than the banking industry. One of the ‘mantras’ of shareholder capitalism is to be among the top three players in the industry. This has led to a lot of consolidation, not always good.

Other perceived weaknesses of shareholder capitalism are ESOPs and stock buybacks. Senior management usually get a big chunk of Employee Stock Options (ESOPs) and are thus incentivized to drive up the stock price. QE, quantitative easing, meant to provide low cost funds for companies to invest, and consumers to buy, was used by corporate management to borrow and buy back company stock, driving up its price, and the value of their stock options.

In other words, whilst China was investing in new technologies, and now leads in 37/44 of them, USA was investing QE money in stock buy backs to enrich top management. Its no surprise that USA has a high GINI coefficient, at 41.4 versus China’s 31.8. Moreover, USA was also spending enormous sums on wars. The Afghan war cost it $ 2 trillion, lasted 20 years, and ended in an ignominious retreat.

So, we have now reached a point where USA has reached a debt ceiling, which can restrain its ability to borrow more, and invest more to bridge the lag in technology development. The Fed has announced its intention to raise interest rates higher, as inflation remains stubbornly high. That raises the cost of servicing its debt. The figure of $ 31 trillion of debt doesn’t included unfunded pension obligations. Pension funds need to be topped up, but can’t (no money) as the returns on those funds are insufficient to meet obligations. France, also facing the same problem, is trying to raise the retirement age (so that pension obligations get delayed) but unions are publicly protesting.

The higher for longer interest rates stance of the US Fed will delay the end of the bear market.

Last week the sensex closed at 59135, down 573.

India continues to spend on much needed infrastructure, such as the Rs 124,000 crores Dedicated Freight Corridor (DFC). Hitherto both passenger trains and freight trains shared the track. Were they to cross, it was the freight train which needed to stop, thus adding both time and cost to logistics. High logistic costs make Indian goods less competitive in Export markets. Two initiatives to reduce logistic costs are DFC and the Inland Waterways projects.

The India story looks good, except for the clogged judicial system, with grant of interminable adjournments, displaying a callous disregard to delayed justice.

In the US and now also in India, bond markets have flashed a warning, by inverting the yield curve. Yields on shorter duration bonds are higher than those on longer duration bonds. This normally results in a recession. Rising interest rates also signal one.

Caution is advocated.

Picture source: https://in.pinterest.com/pin/416020084302666902/

Comments may be sent to jmulraj@asiaconverge.com

{kind=link}

COMMENTS