Policy Watch:

Gold has not lost its allure

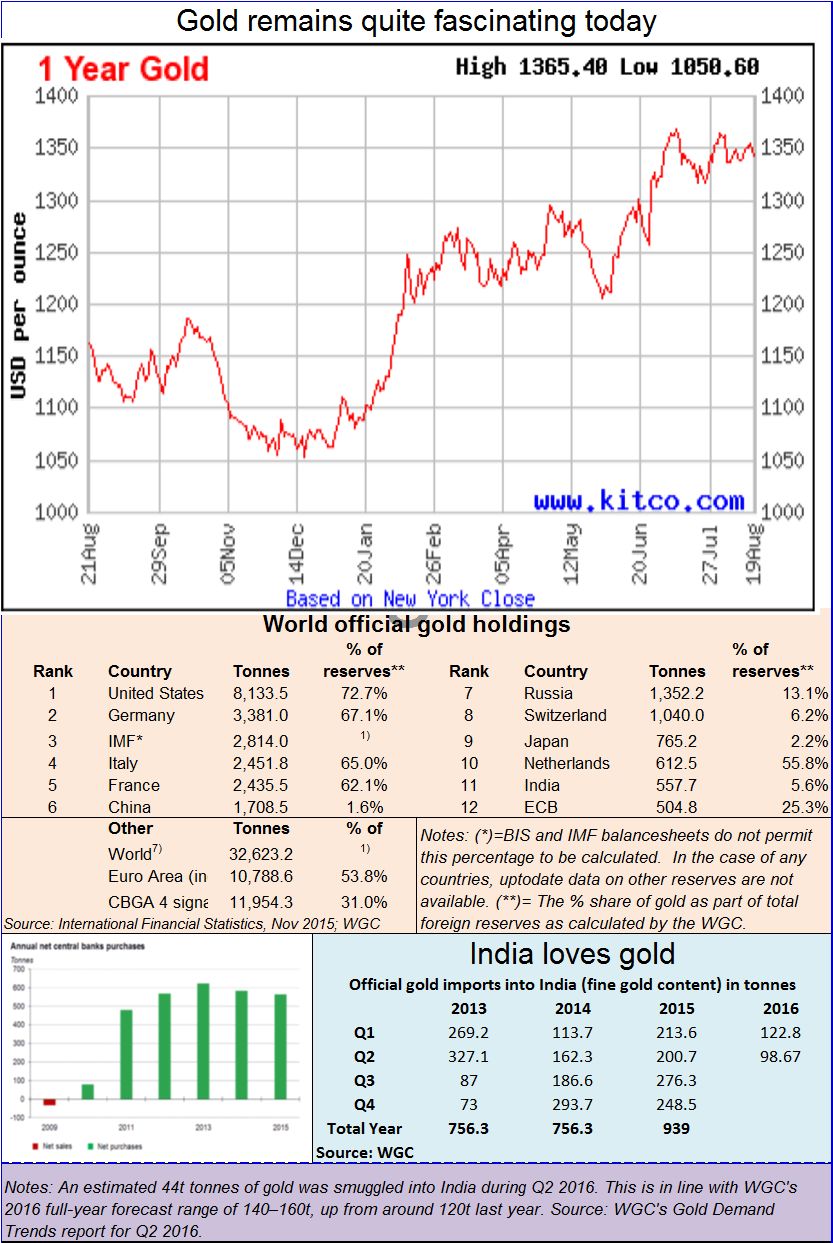

Gold continues to fascinate and perplex. Unlike as during the earlier two decades, central banks the world over have been net purchasers of gold. Earlier they were net sellers. Most analysts believe that the decision to increase gold holdings is the direct outcome of the world’s discomfort with most investment options.

First, the bounce-back of the US has not materialized. Although Walmart posted better than expected results, those posted by other retail chain stores do not inspire. Macy’s announced that it would be closing more than 100 stores. GAP is planning to close around 50 stores. JC Penney registered weak sales and reported another quarter loss. The data posted by Target and Nordstrom did not enthuse analysts either. Obviously, everything can’t be blamed on Amazon and e-commerce portals! There is something else that is afoot here.

First, the bounce-back of the US has not materialized. Although Walmart posted better than expected results, those posted by other retail chain stores do not inspire. Macy’s announced that it would be closing more than 100 stores. GAP is planning to close around 50 stores. JC Penney registered weak sales and reported another quarter loss. The data posted by Target and Nordstrom did not enthuse analysts either. Obviously, everything can’t be blamed on Amazon and e-commerce portals! There is something else that is afoot here.

So what gives? The credit bubble is growing bigger. As Jocelyn Smith, senior managing editor, Sovereign Investor, points out, New York Fed data shows that U.S. household debt jumped by $35 billion to total $12.3 trillion in the second quarter this year. Bulk of the increase came from auto loans and credit cards. Outstanding debt had dropped by $1.5 trillion between 2008 and 2013. But now it is back to 2008 levels. The discomfort is understandable.

Second, China hasn’t recovered either. It looks that there will be a bit more of pain on that front, before things begin to look brighter.

Banks in most countries in the EU have begun opting for ZIRP (zero interest rates) or even NIRP (negative interest rates). Banking is being turned on its head (http://www.freepressjournal.in/nirp-and-the-rosy-indian-economy/862987). However, instead of spurring consumer spending, it has made people flock to gold.

In India, however, consumer demand fell in the first half of 2016. As Somasundaram PR, managing director, India, World Gold Council (WGC) explains, “In India, consumer demand fell 18% to 131 tonnes in Q2 2016, compared to 159.8 tonnes in the same period last year, and only marginally higher than Q1 2016. This quarter too was a truncated period for sales as the jewellers’ strike extended into April and remained more or less effective until Akshaya Tritiya, when sales saw a brief boost. However, elevated price levels and a regulatory push for transparency through PAN cards, tax collection at source and excise duty on jewellery, coupled with weaker rural incomes kept demand subdued.”

But the second quarter witnessed a spurt in the flow of unofficial gold into the country, significantly impacting the organised and tax compliant segments of the gold industry. Moreover, WGC expects gold demand to bounce back to “normalcy” in the second half of this year. It estimates estimate gold demand for 2016 to be in the range of 750 to 850 tonnes.

Available data appears to show that gold demand in India is likely to continue to remain strong (see chart). Even globally, WGC data shows that demand in Q2 soared. Huge ETF inflows were counterbalanced by anaemic jewellery demand amid rising prices. But investment was the largest component of gold demand for two consecutive quarters – the first time this has ever happened.

It looks as if consumer demand for gold is not likely to falter, in India or globally.

If India wants to reduce its gold import bill, it must move more aggressively with its gold monetisation schemes but in a customer friendly manner. The present schemes are too stodgy and cumbersome. It is time the government and the RBI revives its interest in the KUB Rao report (https://rbi.org.in/scripts/BS_PressReleaseDisplay.aspx?prid=27890) submitted in January 2013. The report recommended the setting up of a separate regulator for gold, under ‘The Bullion Corporation of India’ (pg 63 of that report). That would free this metal from the direct control of the ministry, and would allow for a more professional and market friendly approach towards gold. The government has done this for mutual funds and other commodities. It is time to have an independent regulator for gold.

That gold is the flavour of the season is best is discernible in gold speculative markets. You will come across punters in Dubai who are predicting gold prices to cross $25,000 an ounce (as against $1,350 at the moment). That may be pure speculation. But it underscores the global mood.

When everything else becomes uncertain and shaky, trust in gold.

{kind=link}

COMMENTS