Yarns government spokespersons spin about jobs and growth

By RN Bhaskar

The government may say that the economy is looking good, and that India is on the rise.

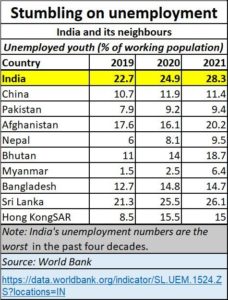

But some key indicators are flashing red. Few jobs, little growth and a bleak future. The government does not want people to look at these grim realities. Abd this is precisely the topic of this video (https://www.youtube.com/watch?v=Laovf2Js0Hg).

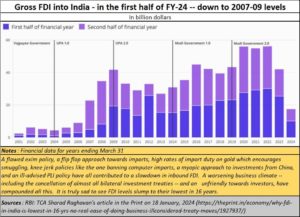

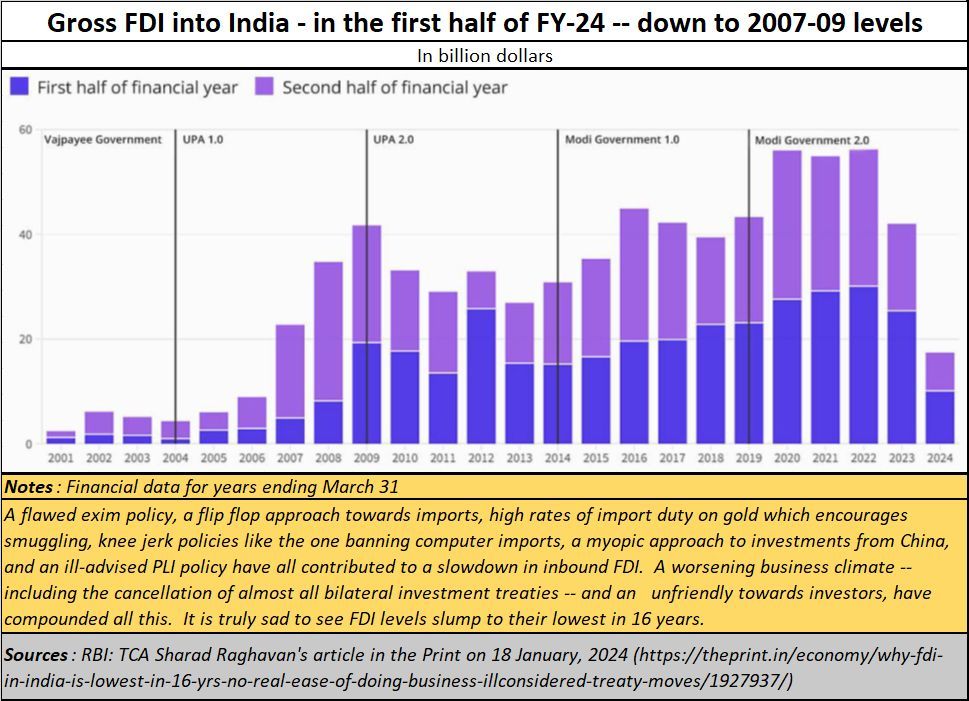

Foreign Direct Investment (FDI) is at a decadal low. It has been dipping year after year. The causes for this are extremely worrying.

Foreign Direct Investment (FDI) is at a decadal low. It has been dipping year after year. The causes for this are extremely worrying.

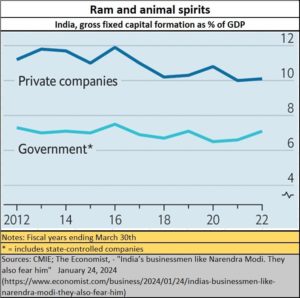

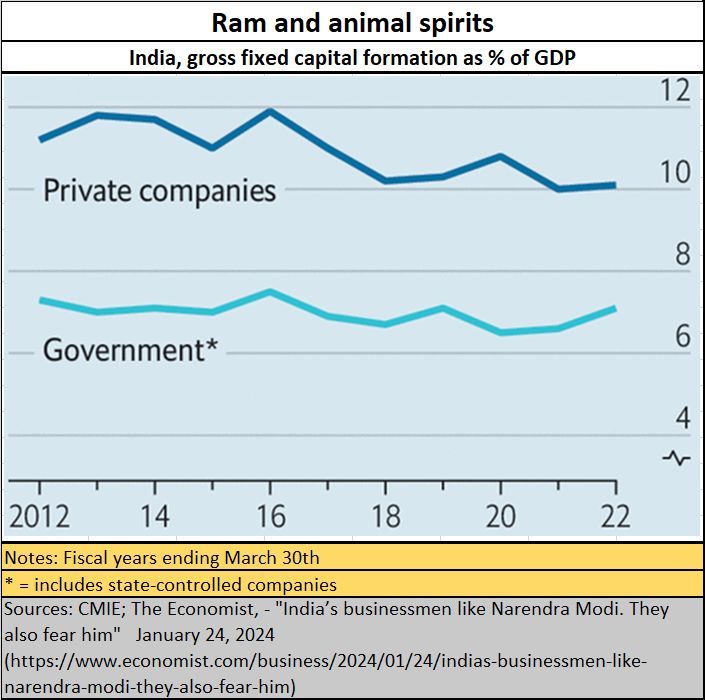

- Poor investments, especially by the domestic private sector and by foreigners (FDI) resulted in fewer business opportunities emerging, which has led to poor job creation. Clearly, building temples is not the answer (Free subscription — https://bhaskarr.substack.com/p/what-after-the-ram-mandir?sd=pf).

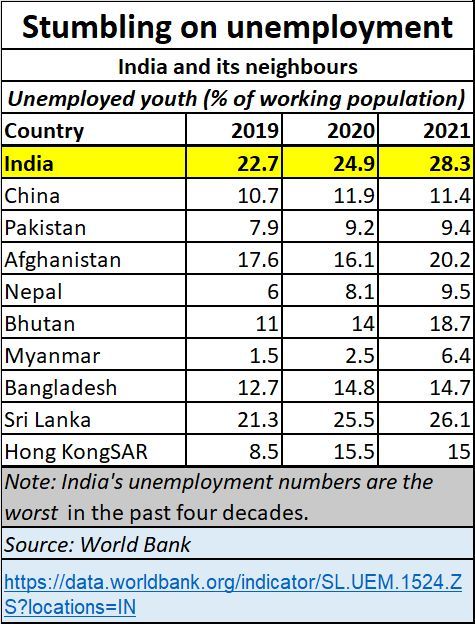

- That in turn has led to poor employment, which is also on account of poor employability (https://www.youtube.com/watch?v=AW2UrnsT9F4). India needs at least 15 million new jobs each year, given its population of 1.4 billion. Jobs can come only if there is growth. That requires investments. Both the private sector and foreign investors are not confident about the investment climate.

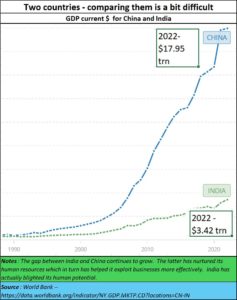

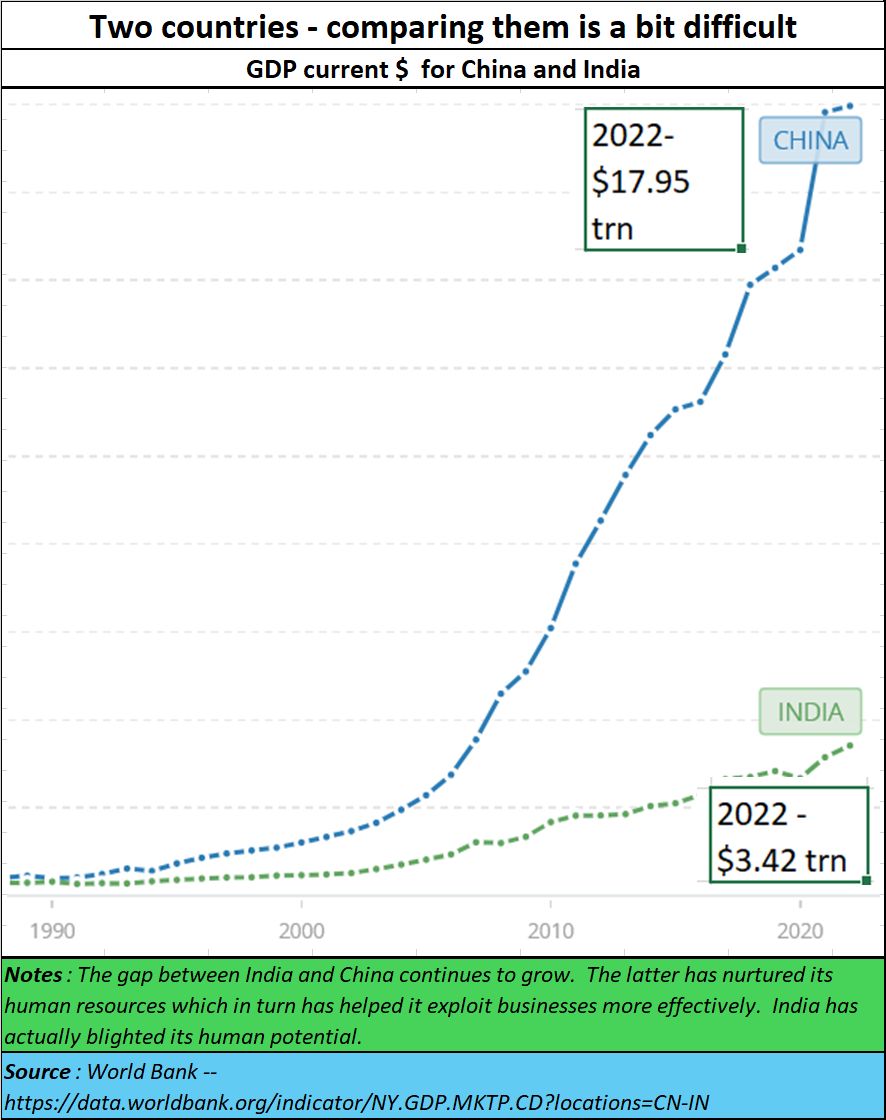

- The government’s comparison with China is grossly misplaced, because China has a GDP of around $18 trillion. A 5% growth means an incremental $ 897 billion a year. Compare this with $171billion for India at 5% growth or $ 274 billion at 8% a year. Someone is clearly fibbing. Moreover, indications are that China is rebounding. More on this later.

- India must realise that mere spending and boosting GDP is not the answer. (https://bhaskarr.substack.com/p/just-look-beyond-indias-gdp-numbers) You can increase GDP by borrowing as well. What is needed is effective investment of these funds into economically viable projects. But the government’s approach to the two dedicated freight corridors shows that populism than economic sense matters a lot more. Consequently, the entire western industrial belt continues to languish because the government wants to push the eastern corridor more aggressively (Free subscription – https://open.substack.com/pub/bhaskarr/p/indias-two-dfcs-politics-trounces?r=ni0hb&utm_campaign=post&utm_medium=web).

In addition to all this, India needs to improve the investment climate. It must allow for international arbitration (https://asiaconverge.com/2020/01/arbitration-and-investment-protection/), which is what major investors want. They do not trust the government’s promises of fair regulation or even the judicial processes involved in this country.

Hypocrisy and bad faith

Hypocrisy and bad faith

Finally, there are two more problems. There is no clear indication that the government is committed to cleaning up the banking sector, or providing a level playing field for financial sector players. Or even in creating jobs and preventing the loss of existing jobs.

One the one hand both the RBI and SEBI have been cracking down hard on parties they claim have violated norms and regulations. That is why both have either grounded or trimmed the wings of players like PayTM, Kotak Mahindra Bank, JM Financial and IIFL Finance.

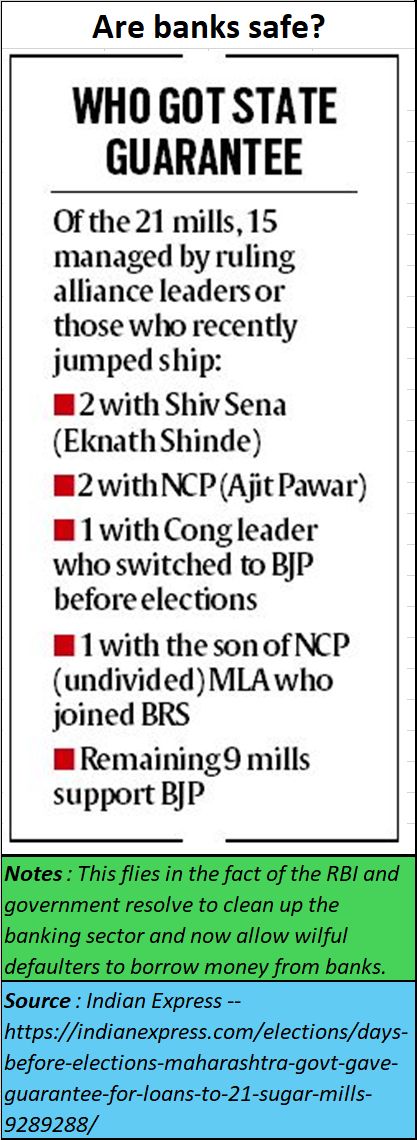

But the RBI looks the other way when the state government of Maharashtra decides to grant bank guarantees to 21 sugar mills just days before elections are due (https://indianexpress.com/elections/days-before-elections-maharashtra-govt-gave-guarantee-for-loans-to-21-sugar-mills-9289288/).

Everyone knows that sugar cooperatives have been defaulting time and again on bank loans, usually guaranteed by the government. Yes, despite their terrible track record, the government gives them bank guarantees for additional loans! And by the looks of what has been reported, the biggest beneficiaries continue to be the politically favoured.

There is a mismatch between the claims of penalising errant players and rewarding politically connected defaulters. In fact, there are stories galore about agricultural mismanagement – but that will be taken up separately.

The other part is the crisis the IT sector faces today. In just one year, over 67,000 jobs have gone just at Infosys, TCS, Wipro and Tech Mahindra (https://www.indiatoday.in/technology/news/story/in-just-one-year-over-67000-jobs-gone-at-infosys-tcs-wipro-and-tech-mahindra-2505495-2024-02-22). Job losses for the Indian IT sector as a whole could be much greater. This is in the face of the surging unemployment in the country. The irony is that the government is unwilling to create outsourcing opportunities to accelerate job formation. The government is, after all, the biggest source of IT jobs that can be outsourced. Look at what happened to the passport sector once it was outsourced. The difference is incredibly amazing. Can it not do this for land records? Or crop mapping (to provide live updates of crop acreage and yields and even food security). Or just focussing on measuring water consumption at all levels – domestic, industrial, and agricultural?

The problem is that the government does not want to do this, because that would usher in more transparency, and squeeze the pockets of illegal gratification which lubricate the political machinery. If the government were serious about employment and wealth generation, this is what it should be doing. It could also promote rooftop solar more aggressively, instead of just paying lip service to this sector (free subscription — https://bhaskarr.substack.com/p/a-new-policy-direction-for-solar).

Yes, India has solutions. But the biggest problem is government and governance. Unless that is set right, expect India to continue to sink. Spinning yearns can be counterproductive.

{kind=link}

COMMENTS