https://www.freepressjournal.in/analysis/policy-watch-can-africa-become-the-new-market-to-stump-india

(The entire series can be found at http://www.asiaconverge.com/2021/05/agenda-for-the-government-2021-series/)

Is it strike #3 for India’s position as an attractive market? Will Africa trounce India?

I deal in facts, not forecasting the future. That’s crystal ball stuff. That doesn’t work.

— Peter Lynch

By RN Bhaskar

This article may appear to be crystal ball gazing. But it is based on facts. And they point to two paths. One leads to an India as a vibrant market. The other to a wasteland.

India has a habit of looking at gift horses in the mouth. It has believed that its allure will last forever, and more and better gift horses will always come along. But like the old story about the spinster who got left behind because she spurned every proposal, confident that a better one would come along, India is now in danger of ending up like the old spinster. It may be all dressed up, but may have nowhere to go.

Three missed opportunities

Just consider three of the most significant gift horses.

Textiles: All through the 1950s to the 1970s, everybody believed that India would remain the biggest player globally in the textile markets. And India’s policy makers thought that they could bring about order and growth into this market. So, they licensed the industry. No industrialist could put in an additional loom without an  explicit written permission from the government. An industrialist was not allowed to convert an old semi-automatic loom for an automatic loom. That is how the Textile Commissioner’s office was born. It spawned a market for intermediaries who could help industrialists with paperwork to be filed and route it through the right officer to procure approval for a loom. The officers and the touts flourished. The nation didn’t. The government’s labour policies made things worse.

explicit written permission from the government. An industrialist was not allowed to convert an old semi-automatic loom for an automatic loom. That is how the Textile Commissioner’s office was born. It spawned a market for intermediaries who could help industrialists with paperwork to be filed and route it through the right officer to procure approval for a loom. The officers and the touts flourished. The nation didn’t. The government’s labour policies made things worse.

The textile industry moved to China, Bangladesh, Sri Lanka, Vietnam, and other places. Today, India’s garment exports barely cross $1 billion compared to almost $34 billion for Bangladesh. One did not require a crystal ball to tell people that India would lose out when bureaucrats tried controlling a market. Like the old Gujarati saying – Jyaan Raja Vepari, Tyan Praja Bikhari (where the king tries becoming a businessman, there the subjects become beggars).

Demographic dividend: Fast forward to the turn of this century. Everyone was gloating about India having the most amazing demographic dividend. Policymakers firmed up their rules on who should run schools, and how higher educational institutions should be run. Ditto for medical colleges as well.

Once again, a crystal ball wasn’t needed. India’s education and health services crashed (http://www.asiaconverge.com/2020/06/blighted-vision-for-healthcare-medical-education/) with a rapidity nobody could have imagined.

Last week confirmed that India’s QS scores remain pathetic as before (https://www.topuniversities.com/university-rankings/world-university-rankings/2022). None of its educational institutes rank among the top 100. Only four Indian institutes of higher learning rank among the top 255 in the latest QS World University Rankings 2022 (#177 for IIT-Bombay, #185 IIT-Delhi, #186 Institute of Science and #255 IIT-Madras). Moreover, India’s education policy have made other countries rich and this country poor (http://www.asiaconverge.com/2020/05/education-enriching-other-countries-pauperising-india/).

The government brought out a New Education Policy – that was a joke (http://www.asiaconverge.com/2020/08/the-national-education-policy-has-little-vision-less-strategy/). India has almost lost its demographic dividend over the past 20 tears. It used to be a land of learning. Today, it is driving education out of this territory.

A booming market: All through the last two decades India kept thumping itself on the chest, trumpeting that it was the second largest market in the world, and would soon become the largest market. It waxed eloquent about the size of its middle class.

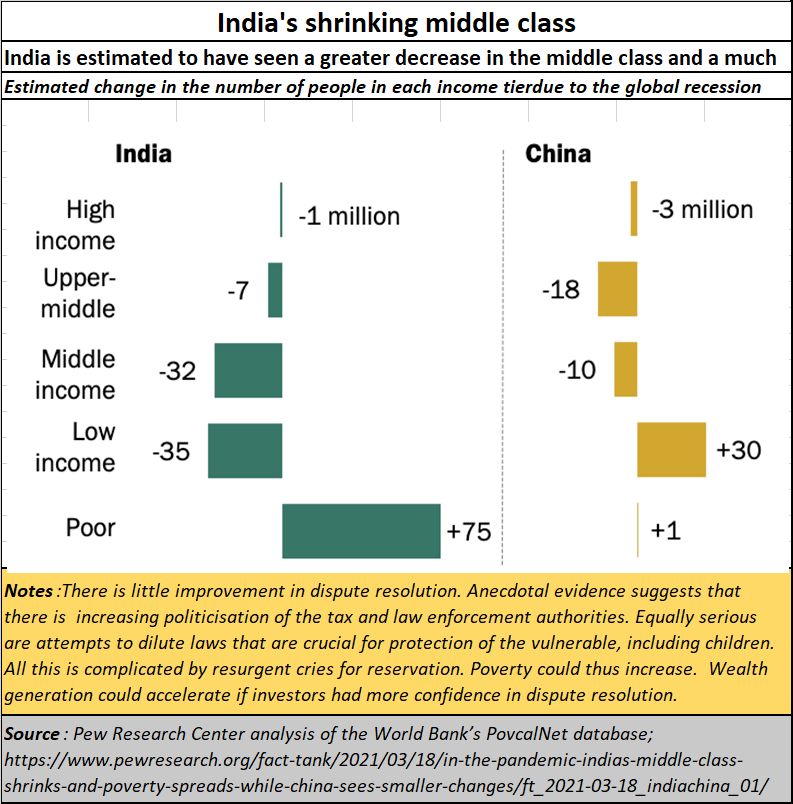

Before the pandemic, it was anticipated that India’s middle class would increase by 99 million people by 2020 (https://www.livemint.com/news/india/indias-middle-class-may-have-shrunk-by-32-mn-in-2020-due-to-recession-report-11616077697955.html).

The first phase of the pandemic was sufficient to slash the middle class by 67 million (https://www.pewresearch.org/fact-tank/2021/03/18/in-the-pandemic-indias-middle-class-shrinks-and-poverty-spreads-while-china-sees-smaller-changes/). The markets shrank (see chart). With almost a third of its middle class gone, it may not have much of a market left by the time the (far more crippling) second wave is over.

Worse, India’s poor have increased by 75 million to reach around 134 million — more than double the 59 million expected prior to the recession. Unemployment is rife, and gross capital formation has stalled.

The government’s argument is that the pandemic is an aberration. India will revive. Maybe, yes. But this aberration hit other countries too, especially neighbouring China. What made India bleed more is that it has nurtured policies to protect the rich, but not the poor. It taught people to live on doles, subsidies and giveaways, and thus made them beggars. It did not allow them to become productive. The government interfered at every step of the way, especially when it came to:

Education (http://www.asiaconverge.com/2020/05/poor-education-kills-million-of-children-each-year/),

Milk (http://www.asiaconverge.com/2021/05/agenda-1-dont-meddle-with-the-dairy-sector/),

Agriculture (http://www.asiaconverge.com/2020/12/farmer-agitations-fueled-by-corruption-politics-and-power/)

Even manufacturing —as evident from the falling PMI (https://www.moneycontrol.com/news/business/economy/services-pmi-falls-for-first-time-in-8-months-as-domestic-demand-disappears-export-orders-nosedive-6981991.html).

Like it did with the textile industry, the government just did not allow enterprise to grow. Lip service, yes. Actual reform, no. Even the PLI (Production Linked Incentives) strategy may be the wrong one to follow, states Arvind Panagariya, former vice-chairman of NITI Aayog (http://www.asiaconverge.com/2021/03/india-may-be-pushing-a-wrong-trade-policy/).

What is most frightening is how “India has plummeted from its position of being in the top ten fastest growing economies in 2016 to 164th (2020 calendar year, according to Statistics Times) in the pecking order, a dramatic fall by any yardstick,” states columnist Anjuli Bhargava in Business Standard while discussing noted economist Kaushik Basu (https://wap.business-standard.com/article/economy-policy/demonetisation-covid-19-brought-indian-economy-to-its-knees-kaushik-basu-121061101499_1.html).

Any alternatives?

Yes, plenty.

Yes, plenty.

Option one – allow investments to pour into India, with recourse to international arbitration and investment protection(http://www.asiaconverge.com/2020/01/arbitration-and-investment-protection/). You cannot expect investors to come to India with no clear route to dispute resolution. At present, the government’s unwillingness to strengthen the judiciary has pushed the country into a corner. Investors are convinced that this country is unreliable when it comes to resolving disputes. The government’s penchant for retrospective legislation has made the situation worse. And instead of correcting its aberrations, it wants to challenge the Devas, Vedanta, and Vodafone cases in international courts.

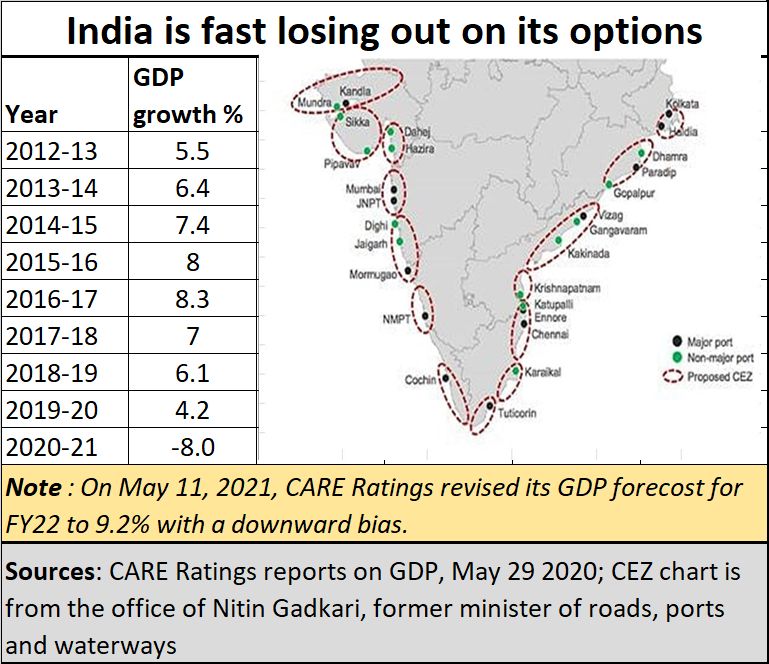

Option 2 – quickly announce CEZ schemes, under the shelter of the Constitution’s provisions for industrial cities (http://www.asiaconverge.com/2021/05/agenda-2-cezs-can-bail-india-out/). This will allow at least these pockets to grow quickly without affecting the way the rest of the country works. Legislative changes can take time. And managing revenue sources and vote banks can be difficult.

Option 3: India does not change, does not move quickly to create jobs and generate money. It fails to expand the middle class. Without jobs, and a resurgent middle class, India will not be the prettiest girl in town. The suitor-investors will begin looking elsewhere.

It is worth recalling the findings of the Nomura study which effectively punctured India’s faith that companies leaving China would opt for India. The report showed that of the 56 companies that sought to move out of China as labour costs were climbing, only three came to India (http://www.asiaconverge.com/2020/05/investments-land-smallest-part-problem/). The rest went to other countries like the Vietnam, Taiwan and Thailand and other countries.

And now there is more attractive prospect that could blossom within the next 5-10 years. If India does not move fast, its goose will be cooked.

The competition

It does not look like competition today. It has major governance issues. But it could be the proverbial ugly duckling. And like the  story, this duckling could become a swan. The contender is Sub-Saharan Africa (SSA).

story, this duckling could become a swan. The contender is Sub-Saharan Africa (SSA).

What? Not possible!

Just look at the numbers.

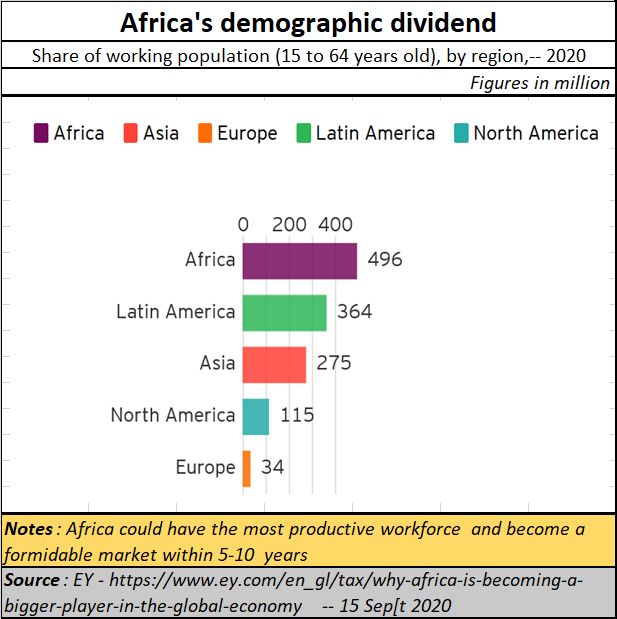

The first chart shows the SSA as one of the sweetest spots when it comes to demographic dividend – something that India enjoyed two decades ago.

It still does, but its population has abysmal education – literacy is still calculated on the basis of anyone who can read or write his or her name.

It has the most depressing of graduates – barely 20% is employable. If international law firms are asked, barely 1% of the graduates is employable.

Its medicare system is terrible – as the recent deaths in the second wave of the pandemic have shown.

India’s phase of demographic dividend is coming to an end. Its markets are shrinking, unless jobs are created, and investments are attracted (https://www.nature.com/articles/s41599-020-0529-x). And this is again where Africa is sharpening its edge (see chart).

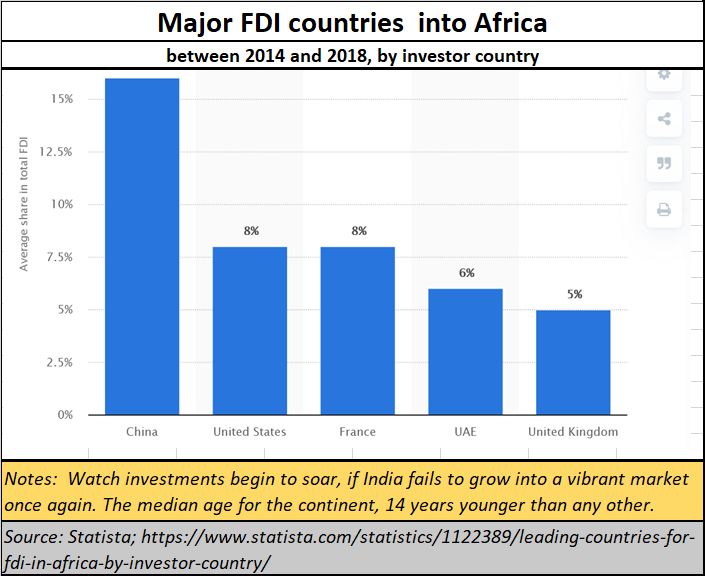

True, China is a big investor because it is keen on the commodities that SSA offers. So what? All investors look for some reason to invest. Some for production. Some for commodities. Others for trading. India could offer the benefit of production, but not when states want reservation for their own people, or the centre wants reservation for backward classes. And judicial redressal is a nightmare.

The objective of investors is to gain from productivity. That is again another reason why the CEZ offers a good temporary solution. Eventually, the entire country should become a special economic zone, without the police raj and the attendant corruption. But let’s start with the CEZ.

The objective of investors is to gain from productivity. That is again another reason why the CEZ offers a good temporary solution. Eventually, the entire country should become a special economic zone, without the police raj and the attendant corruption. But let’s start with the CEZ.

To market, to market

And do remember that the entire world needs a market to grow, to survive, to thrive. If India cannot make market access easy, then they will go about creating a new market. It is worth noting that 30 years ago, the US wanted a market, and India was unwilling. So, it, along with other countries, looked at China. What they did not expect was that China would grow extremely well. It has now become the biggest market in the world, and also the biggest producer and exporter. The west is in decline, and China is in the ascendant.

So why should India try to ban China? Why block its investments into India? India’s policymakers must be truly myopic or suffer from a death wish. And if China is thwarted by India, it will work on growing Africa. And this time, even the US and EU will support China. All will have a common interest – creating a new market. India may cease to be considered attractive in five years’ time.

Listen to the World Bank (https://www.worldbank.org/en/region/afr/overview): “Sub-Saharan Africa, home to more than 1 billion people, half of whom will be under 25 years old by 2050, is a diverse continent offering human and natural resources that have the potential to yield inclusive growth and eradicate poverty in the region, enabling Africans across the continent to live healthier and more prosperous lives. With the world’s largest free trade area and a 1.2-billion-person market, the continent is creating an entirely new development path, harnessing the potential of its resources and people.”

At 1.2 billion people, it is almost the same size as India, but with a more aspirational population. India needs to wake up fast. Keep the smelling salts ready because the tensions could make India’s policymakers sick.

At 1.2 billion people, it is almost the same size as India, but with a more aspirational population. India needs to wake up fast. Keep the smelling salts ready because the tensions could make India’s policymakers sick.

Another interesting, though counter-intuitive fact is that SSA has learnt to manage downturns better than India has. So, while India shrank by 8% during the first wave, SSA shrank by just 2% in 2020, says the World Bank.

Yes, Covid-19 has plunged the region into its first recession in over 25 years, with activity contracting by nearly 5% on a per capita basis. But, again as estimated by the World Bank, “In East and Southern Africa, the growth contraction in 2020 is estimated at –3%, 0.9 percentage point less than projected in October 2020, mostly driven by South Africa and Angola—its two largest economies. . . . . . Sub-Saharan Africa’s recovery is expected to be multi-speed, with significant variation across countries. . . . . Faster progress on vaccine deployment along with credible policies to stimulate private investment would accelerate growth to 3.4% in 2021 and 4.5% in 2022.”

Africa transformed?

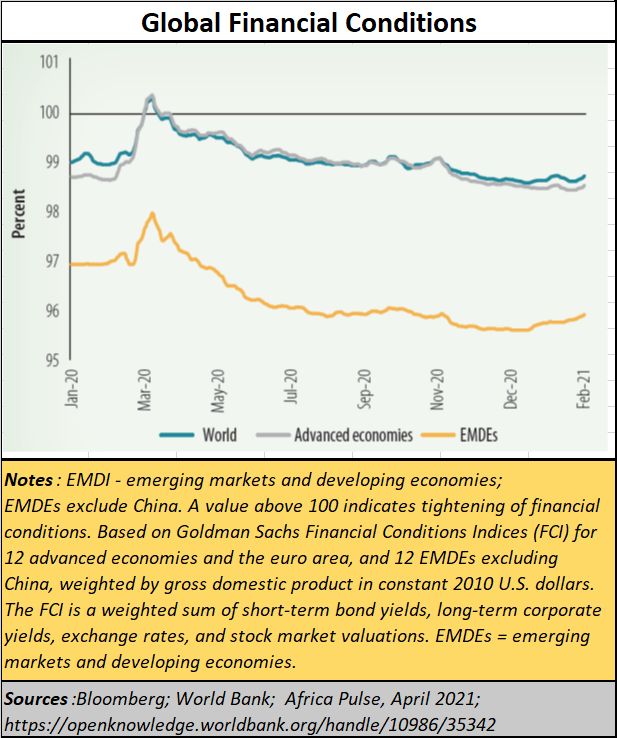

Moreover, as the chart alongside shows, global growth will continue to be dependent on emerging markets and developing economies (EMDI). India still has the edge. Its youthful charms are diminishing. Its wrinkles are showing. Few have the patience to deal with its pouts and petulance.

Consequently, it should move fast. But if it tries to play hard-to-get, or act recalcitrant, investors will begin looking at other attractions. SSA is the most desirable of them.

It is also worth considering what the World Bank had to say in Africa Pulse report of 31 March 2021 (https://www.worldbank.org/en/publication/africa-pulse).

The SSA is not wasting the opportunity from the COVID-19 crisis, [the countries] are increasingly adopting digital technologies to boost productivity in current jobs, and increase employment opportunities, particularly for women and youth. “To unlock the full benefits of a digital economy, the report recommends policies that accompany investments in digital infrastructure such as a regulatory framework that fosters competition and innovation in telecommunications, provision of reliable and affordable electricity, investment in education and upgrading the skills of informal workers,” adds the World Bank.

To conclude – with little of demographic dividend left, with its key industries like textiles and even milk under threat from constant government interference, and with its middle class shrinking alarmingly, India needs to create jobs desperately. For that it needs large investments. That requires confidence in dispute resolution and insulation of the caprices of an inspector raj.

If India does not warm up to investors, it will end up like the spinster, who once had dreams of great days.

{kind=link}

COMMENTS