4 July 2026

India shouldn’t be harsh with serious investors

By RN Bhaskar and Sakeena Bari Sayyed

Image: Copilot

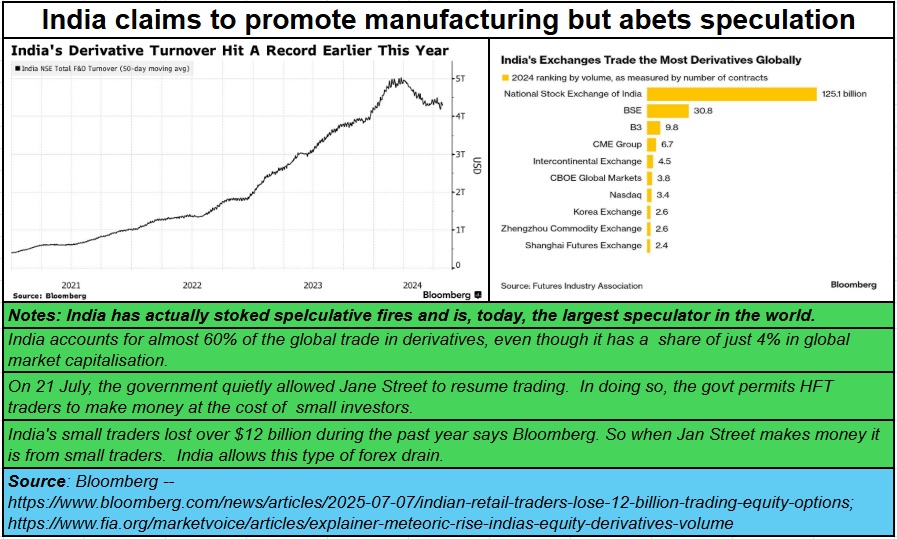

By now, it is increasingly clear that India has been more fair to foreign investors – especially speculators – than Indian investors. Indians are taxed on investments. There is capital gains tax, the Security transaction tax (STT), and there is income tax too. Foreign portfolio investors have just been exempted from such taxes. Such laws already created havoc in the past (remember the Jane Street affair — https://www.bbc.com/news/articles/c5y0zgrevl1o?). India is guilty of being more liberal with speculators than genuine investors. And among speculators, it loves foreigners more than Indians. As a result, it has allowed more money to flee India than it has encouraged money to come into India.

By now, it is also quite evident that the government cares little for the niceties of law. That is another reason why money flees India.

By now, it is also quite evident that the government cares little for the niceties of law. That is another reason why money flees India.

Its recent observation that passports are not proof of citizenship, but that it is merely a travel document, has stunned most people (https://www.youtube.com/live/A_-pMXfC-Dk?si=1q2jz0znSh5LJwnV). Globally, a passport is the ultimate proof of citizenship, unless it can be withdrawn, seized or impounded by the authorities according to the provisions of law. That disregard for laws is one more factor that investors will carefully consider before deciding to invest in India.

The need

This is despite the glaring fact that India needs investors badly. India’s disdain for law is extremely vexatious. India’s disregard for the rights of investors became evident when it decided to scrap almost all BITs (bilateral investment treaties) in 2014 (https://asiaconverge.com/2020/01/arbitration-and-investment-protection/). The reason? The government did not like the idea of foreign investors approaching international arbitration councils to decide on matters that Indian courts were supposed to.

That would not have mattered had the Indian courts taken legal disputes seriously, and had settled the source of vexation speedily and judiciously. Unfortunately, India has a reputation for dragging out cases, which investors do not like. Any delay in dispute resolution makes the culprit stronger, and the victim weaker.

In fact, it was the way Indian courts handled a matter involving an Australian company that resulted in the shameful development where India was hauled up by the courts in Singapore. To remedy that, India’s Supreme Court agreed to allow foreign investors the right to international arbitration. Even this is sought to be circumvented.

Anti-investor rulings

The Indian government cancelled 56 BITs. It wanted countries to sign a fresh BIT which stated that foreign investors would not approach international arbitration centres will they had exhausted legal options in India. But that could take forever. Predictably, no country agreed to sign the new BIT format, except for two countries — Cambodia and Belarus. Both are countries which have few trade ties with India. Effectively the revised BIT did not matter for these two. Even today, the one issue on account of which the EU will not sign an FTA with India involves the right to international arbitration.

After 12 years, the government now appears to be looking closely at a new format which will allow foreign investors to approach international arbitration centres after trying out Indian courts for two years. But even that is uncertain (https://www.freshfields.com/en/our-thinking/blogs/risk-and-compliance/indias-investment-treaty-landscape-in-2026-102mmwp).

As Freshfields points out, “A revised Model BIT is under consideration, but its content remains unknown. India has confirmed that revisions are underway to its Model BIT, which will be “more investor-friendly”, but no draft has been released. India’s new trade agreements do not confer arbitration rights on foreign investors.” Instead, points out Freshfields, “India has continued to exclude investor-State arbitration, channelling any disputes through State-to-State mechanisms only.”

Thus, the first requirement for making India an investor-friendly nation is by improving dispute resolution and allowing arbitration (https://asiaconverge.com/2021/03/the-judiciary-series/). But that will be difficult, if the basic structure of the judiciary is not made stronger. But that would fly in the face of the government’s own desire to weaken the Indian judiciary. The manner in which it has promoted judicial corruption is both deplorable and horrifying (https://asiaconverge.com/2026/03/why-governments-love-to-corrupt-judiciary/).

Still defiant

Indian politicians don’t like a strong judiciary. That is what all indicators that have been referred to above seem to suggest.

We need forex urgently

We need forex urgently

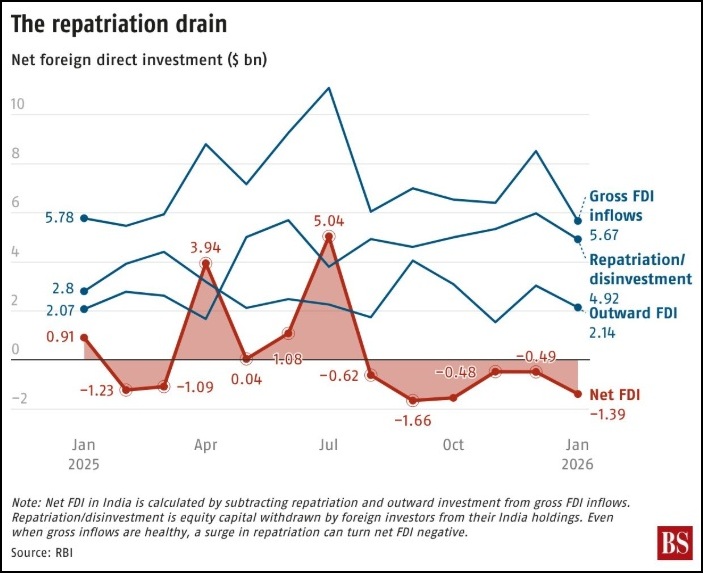

But these are desperate times. India’s net FDI has already turned negative. And there appears to be a flight of capital.

Unfortunately, times are likely to get even more desperate. Fuel and fertiliser prices are likely to soar (thanks to the Middle East wars). A severe El Nino effect will hit agriculture badly (https://www.youtube.com/live/hp_GDoll4Ig?si=tx-HRgtlQSjbxyaK). Over 50% of India’s population has its fortunes yoked to the rural sector, which in turn means agriculture. Unemployment has been increasing relentlessly. A weakening rupee makes the situation worse (https://www.youtube.com/watch?v=sWOMXIAlM2c). Adding fuel to the fire that is already blazing are the government’s senseless gold import rules (https://www.youtube.com/watch?v=Tg-q0x6v2YM). Topping the rot is the rising corruption.

- India’s examination system is in doldrums

- Its chief ministers have gone about acquiring land in shameless ways.

- Even the most prominent project of the government – the Ram Mandir (the temple dedicated to Lord Ram) is filled with the stench of corruption.

- And this does not include the collapse of bridges, potholes on roads and other infrastructure failures (https://www.youtube.com/watch?v=GJpKwcDvw54&t=132s&pp=0gcJCUwLAYcqIYzv and https://asiaconverge.com/2025/11/a-bridge-too-far/).

All these eventually result in higher taxes and more demands for bribes from companies and individuals. It is not a happy picture.

The way out?

- As mentioned earlier, the first thing the government should do is to drop all charges against financial ‘absconders’ once they settle past dues. India will need their skills to bring in investments, and to generate jobs (https://bhaskarr.substack.com/p/the-curious-case-of-indias-financial). It is also important to preserve value of assets seized, rather than allow them to go to seed.

- Focus on giving incentives to domestic investors, not to foreign portfolio investors (FPIs). The former will ensure more jobs get created. The latter just create a froth in the market and take their money away at the slightest whiff of the rupee weakening, the trade balance growing, or the global relevance of India declining. A weakening rupee only helps politically affiliated parties who have stashed their ill-gotten gains. They get more rupees for the money they have taken out of India.

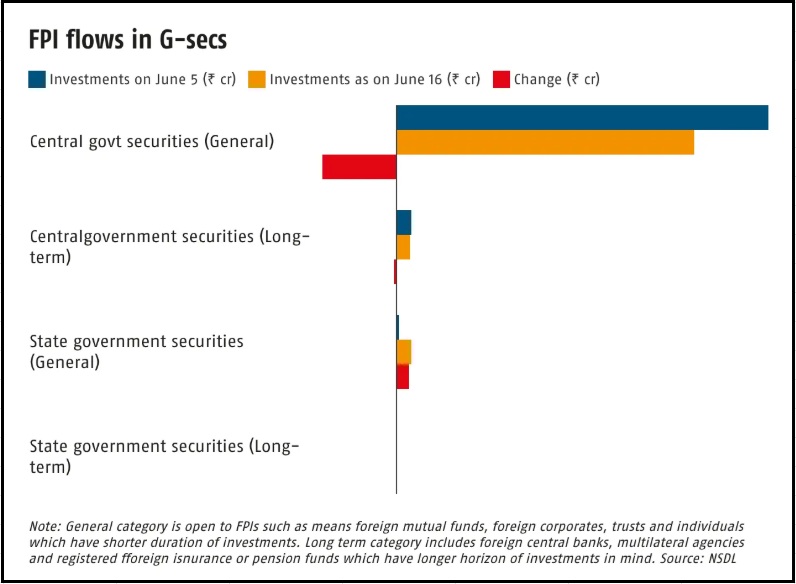

As a Business Standard report points out, only FPIs have been exempted from some taxes on government securities (G-secs) capital gains tax and income tax on interest income on G-secs. The government also removed specific restrictions on short-term investments and security concentration for foreign investors. However, overall investment caps were retained: 6 per cent for central government bonds and 2 per cent for state government securities. General and long-term investment limits were merged into a single cap for both central and state bonds (https://businessstandard.substack.com/p/g-sec-tax-break-yet-to-impress-foreign).

- As Business Standard points out, the government “announced the measures on June 5, effective from the beginning of FY27. But FPIs were not impressed. They withdrew more than Rs 11,000 crore from central government papers and Rs 1,800 crore from state government bonds between June 5 and June 16.”

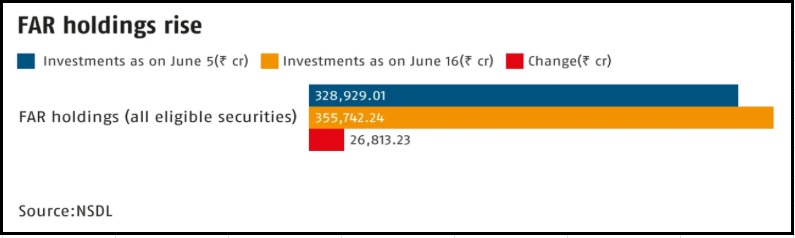

- The government also expanded the Fully Accessible Route (FAR) to include new 15-, 30- and 40-year bonds, as well as Sovereign Green Bonds. True, this appeared to work. “FPI investments under FAR rose by around Rs 27,000 crore between June 5 and June 16. However, their overall share in the FAR universe actually slipped to 6.88 per cent of the outstanding stock as of June 16, down from 6.97 per cent on June 5. Meanwhile, the 40-year government bond failed to attract any FPI investment under FAR,” says Business Standard.

- Compare this with China, where domestic investors are given favourable treatment to encourage them to invest. Timeline 54.45 to 55:20 — https://www.youtube.com/watch?v=O58PYAiOLjs . True, investors in H shares in Hong Kong have not done well, but domestic shareholders in China who cannot take their money out have done marvellously. So Chinese shareholders keep investing in stocks. Thus, for domestic investors there is a booming market. Why can’t India learn these lessons? The only explanation could be that politically favoured people can take their money out and invest overseas or even invest in India as FPIs.

If the same incentives had been given to domestic investors in India, the results could have been startling. That could have led to a more robust economy.

Stop looting banks and the RBI

- Restrain the urge of fleecing the RBI. The government’s temptation of sucking money out of public sector companies and even the RBI must stop (https://bhaskarr.substack.com/p/options-before-the-govt-ii-economy) . In most large scams where money was siphoned off from banks, the government’s involvement is quite visible (https://bhaskarr.substack.com/publish/posts/detail/202802184). This must stop.

- Focus on value. Since energy will be the key requirement, accelerate sensible policies for solar power and nuclear power. The former is important because it can be an employment generator. The Prime Minister made a lot of song and dance about ensuring 1 crore solar rooftop systems in villages (https://www.youtube.com/watch?v=dnsYR9Jcdp8). That promise has also been forgotten like so many others. As a result, the country loses money through long distance transmission lines and a system of subsidies aimed at wooing voters, not strengthening the economy.

Rethink agriculture.

The world will see lower agricultural output in the coming year – maybe for the next four years – thanks to degraded farmland, less fertilizer availability, and poor rains (on account of the severe El Nino factor).

- What will work at such times is hydroponics — https://asiaconverge.com/2018/06/hydroponics-could-be-the-future-of-farming/. That will require more investments. But it is the safest way to insure farmers against climate change, water consumption and fertiliser prices. If handled well, superior controls on nutrients used, and the virtual elimination of pesticides, could ensure a huge market for agricultural exports. Will the government listen?

- Get Food Corporation of India (FCI) out of procurement of grains. Let the FCI procure them from the commodity exchanges (the e-mandi) Let farmers discover prices through the commodity markets (https://asiaconverge.com/2021/08/poverty-in-uttar-pradesh-and-bihar-is-not-accidental/). The government’s policy of protecting the FCI turf has resulted in rich farmers becoming richer and poor farmers facing greater distress. The ability to sell crops on the basis of futures prices would have helped. Now they are compelled to sell at distress prices. One of the causes for poor rural consumption demand is this policy of protecting the FCI.

- A second reason is banned forward markets for the largest number of agrii products in India’s history (https://asiaconverge.com/2022/10/the-folly-of-banning-futures-trading-in-commodities/).

- A third reason is the introduction of the cattle slaughter laws which has crippled milk production in states that embraced cattle slaughter laws (https://asiaconverge.com/2025/03/dairy-ruminations-that-make-little-sense/). The state government of Tamil Nadu has now taken this matter to the Supreme Court (https://www.youtube.com/watch?v=794SNg1qfU0).

The China factor

Do not ignore China. It is investing in Iran – some $400 billion. Much of this will be in Iran’s infrastructure (https://bhaskarr.substack.com/publish/posts/detail/197954130). If India cannot match such investments, it will remain marginalised. Listen to Pravin Sawhney at https://www.youtube.com/watch?v=RxPd8m2hPEs .

Housing for growth

Housing for growth

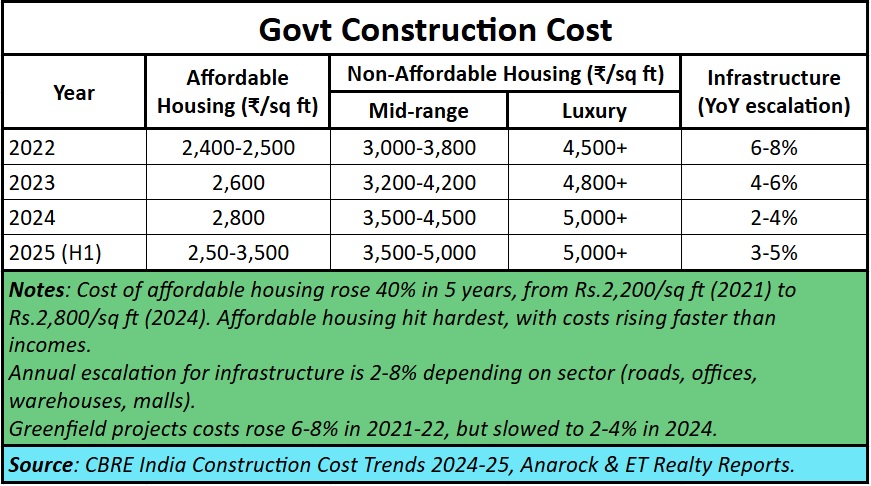

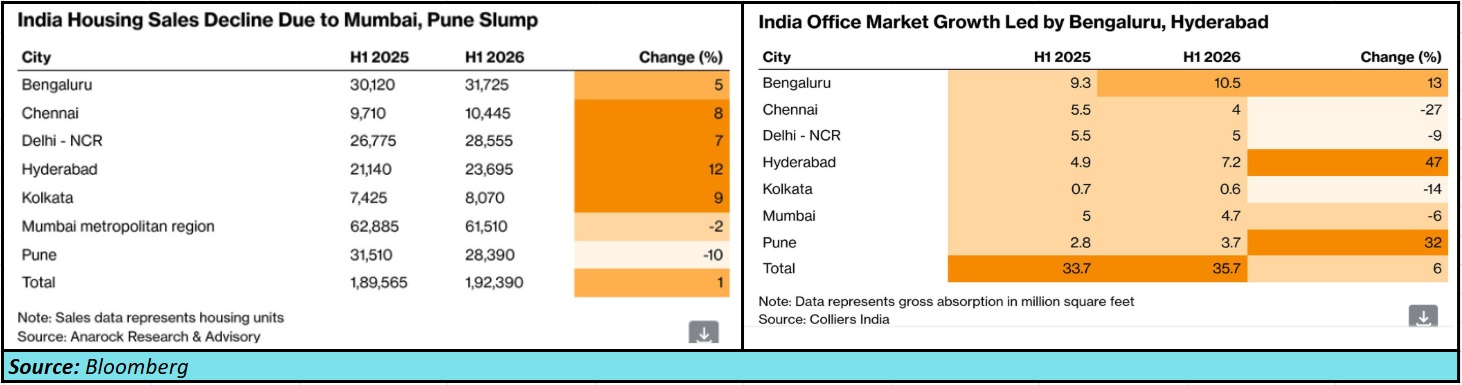

Finally, do a rethink on real estate. The demand for affordable housing is immense. The policies of the government (including state governments) have ensured that real estate is provided to people in dribbles. That creates a sense of scarcity. That in turn encourages a market for corruption, entitlement for the favoured, and high property prices. Learn from Iran and the way it used real estate development to cope with the severest of sanctions from the West (https://asiaconverge.com/2015/11/housing-lessons-from-iran/).

Just look at how property markets are sagging. Less corruption could shave off 40% of the costs. Ensure easy availability and better laws relating to property taxes (Mumbai allows some of the best properties in the city to fetch rents that even slum dwellings cannot command). Introduce more investment friendly rental laws. Abundant supply and good rental laws will allow a rental market to blossom.

Encouraging portents

Encouraging portents

There are some encouraging signs that these desperate times have finally compelled the government to move out of its complacency. It has begun talks with China.

And unknown to many, India has also begun talks with Pakistan. Both talks are aimed at finding ways to coexist. At least three meetings have been held between India and Pakistan at locations in the Middle East. The Indian team comprises retired generals, IAS officers and (wonder of wonders) senior representatives of the RSS (https://www.aljazeera.com/news/2026/5/23/are-india-and-pakistan-quietly-preparing-to-restart-dialogue).

If these talks bear fruit, the outcomes should help reduce expenditure on military purchases and employment. It should also usher in the zone of peace that Xi JinPing talked about when it met prime minister Modi in Tamil Nadu in 2019 (https://www.thehindu.com/news/national/xi-mooted-trilateral-partnership-with-pak/article29713793.ece). It has taken India a long time to come to recognise the advantages of creating this zone of peace.

=============

Watch our latest podcast on the way India has bred more Epsteins than even the US. You can find it at https://youtu.be/wReUS-iWUmQ

=============

Do watch our podcast on India’s security concerns. This time it is on the Indus water featuring Lt Col JS Sodhi (Retd) & Parjanya Bhatt. You can find it at https://www.youtube.com/live/nG0AfMjVsl4?si=kBYas7uD03-wPDDE

=============

Finally, do view our News Behind the News:

- Corruption & theft scams rock the nation

- Land grab is a favoured political route for corruption

- India GDP could fall but Taiwan could be badly hit

You can find it at https://www.youtube.com/live/Y21tSgpEMxg?si=vDr3S2KzU75MiNU0

=============

{kind=link}

COMMENTS